English

English Français

Français 日本語

日本語 中文

中文Annual production of 785,000 ounces of platinum, palladium, rhodium

and gold estimated in base-case operation of 8 million tonnes/year

The Platreef mine is projected to be Africa’s lowest-cost producer

of platinum-group metals

Estimated base-case after-tax NPV of US$1.6 billion

and IRR of 14.3%

JOHANNESBURG, SOUTH AFRICA – Ivanhoe Mines (TSX: IVN) Executive Chairman Robert Friedland and Chief Executive Officer Lars-Eric Johansson today welcomed the positive findings of an independent, preliminary economic assessment of the company’s major Platreef Project in the heart of South Africa’s Bushveld Complex, the world’s premier platinum producing region.

The Platreef Project is a Tier One discovery by Ivanhoe Mines’ geologists of platinum-group elements, nickel, copper and gold, which contains the Flatreef underground deposit, on the Bushveld’s Northern Limb.

“Completion of the Platreef preliminary economic assessment is another significant step in the progression of our plan to develop this remarkable discovery into a world-class, underground mine,” said Mr. Friedland.

“We’re looking forward to working with all of our stakeholders to advance the Platreef Project to production, to create valued and skilled jobs and to significantly contribute to the socio-economic development of the people of area communities who will have a voice in decision making and a direct share in our success through our responsively structured, broad-based, black economic empowerment partner.”

Highlights of the preliminary economic assessment (PEA):

- Development of a large, mechanized, underground mine is planned through a phased approach.

- Three run-of-mine production scenarios were examined – 4 million tonnes per year (Mtpa); a base case of 8 Mtpa; and 12 Mtpa.

- An initial 4 Mtpa scenario would establish an operating platform.

- Options available to accelerate expansions to the base-case 8 Mtpa and also the 12 Mtpa scenarios, as the market dictates.

- Opportunities exist for additional phases of development beyond 12 Mtpa, subject to further study.

Key features of the 8 million tonnes/year base-case scenario include:

- Base-case annual production target of 785,000 ounces of platinum, palladium, rhodium and gold. (At an expanded operating scenario of 12 million tonnes per year, the annual production target would be 1.1 million ounces of platinum, palladium, rhodium and gold (3PE+Au)).

- Platreef, with the highest concentration of base metals among Africa’s platinum-group metals producers, would rank at the bottom of the cash-cost curve, at an estimated US$341 per ounce of 3PE+Au, net of by-products.

- Estimated pre-production capital requirement of approximately US$1.7 billion, including US$381 million in contingencies.

- After-tax Net Present Value of US$1.6 billion, at an 8% discount rate.

- After-tax internal rate of return of 14.3%.

The PEA was prepared by report contributors OreWin Pty. Ltd.; AMEC E&C Services Inc.; SRK Consulting Inc.; Stantec Consulting International LLC; Metallicon Process Consulting (Pty.) Ltd.; and Geo Tail (Pty.) Limited. The full technical report will be filed on SEDAR at www.sedar.com and on the Ivanhoe Mines website at www.ivanhoemines.com within 45 days of the issuance of this news release.

The PEA includes an economic analysis that is based, in part, on Inferred Mineral Resources. Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would allow them to be categorized as Mineral Reserves, and there is no certainty that the results will be realized. Mineral Resources are not Mineral Reserves because they do not have demonstrated economic viability.

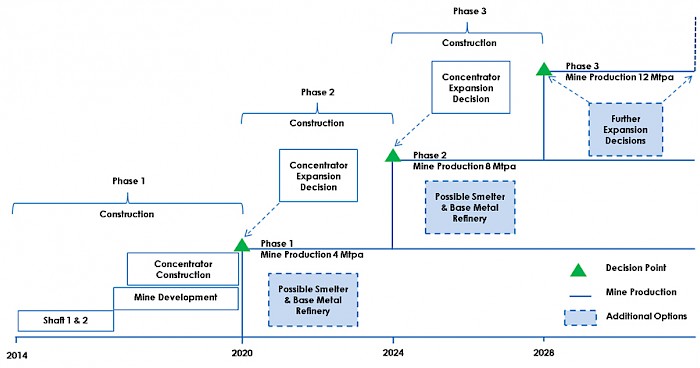

Phased approach to the development of a large, mechanized, underground mine

Ivanhoe’s plan for the Platreef Project considers three phases of potential development for an underground mine and the concentrator processing facility:

- Phase 1 – 4 Mtpa mine and concentrator.

- Phase 2 – 8 Mtpa mine and concentrator (base case).

- Phase 3 – 12 Mtpa mine and concentrator.

The base case for the Platreef PEA analysis is the 8 Mtpa production scenario. The range of development scenarios and additional options for the Platreef Project are shown in Figure 1. The scenarios describe a staged approach, where there is opportunity to expand the operation depending on demand, smelting and refining capacity and capital availability. As Phase 1 is developed and placed into production, there is opportunity to modify and optimize the subsequent phases, allowing for changes to the timing or expansion capacity to suit the conditions at the time. Opportunities for additional expansion beyond Phase 3 may be available, but require additional investigation.

Figure 1: Platreef Project development scenarios.

Source: OreWin

Phase 1 would include the construction of a concentrator and other associated infrastructure to establish an operating platform to support the start of production at a nominal plant capacity of 4 Mtpa by 2020. Phase 2 includes a ramp-up to a plant capacity of 8 Mtpa by 2024; Phase 3 envisages a further ramp-up to a steady-state plant capacity of 12 Mtpa by 2028.

Site preparation is underway for the sinking of the planned exploration shaft to obtain a bulk sample for metallurgical test work. This shaft would form an important part of a Phase 1 project. A Mining Right Application was filed with South Africa’s Department of Mineral Resources in June 2013 and is awaiting approval. When granted, it will permit Ivanhoe Mines to mine and process minerals from the mining area for an initial period of 30 years, which may be extended.

The capital and operating costs for the three phases have been estimated by independent technical consultants and have been included in the economic analysis reported in the PEA. This modular approach has the same underlying plan for the construction and operation of a concentrator processing facility for each phase. The planned rate of mine production will be optimized to supply the progressive expansion of processing capacity in the accompanying concentrator. Infrastructure constructed to support the mine also is common to all phases.

Positive preliminary economic analysis demonstrates Platreef’s exceptional economic potential

The economic analysis uses price assumptions of $8.35/lb nickel, $1,700/oz platinum, $820/oz palladium, $1,300/oz gold, $3.00/lb copper and $1,700/oz rhodium. The prices are based on a review of consensus price forecasts from financial institutions and similar studies that recently have been published. The after-tax net present value (NPV) at a real 8% discount rate, Internal Rate of Return (IRR) and project payback period for each scenario are shown in Table 1.

Table 1: After-tax financial results.

| Phase 1 4 Mtpa |

Phase 2 8 Mtpa (Base Case) |

Phase 3 12 Mtpa |

||

|---|---|---|---|---|

| Net Present Value (US$M) | Undiscounted | 6,992 | 12,527 | 17,078 |

| 5% | 2,040 | 3,593 | 4,818 | |

| 8% | 897 | 1,620 | 2,179 | |

| 10% | 449 | 868 | 1,193 | |

| 12% | 149 | 374 | 554 | |

| 15% | -133 | -77 | -17 | |

| IRR | 13.37% | 14.34% | 14.88% | |

| Project Payback Period | (Years) | 5.59 | 6.40 | 7.55 |

| Exchange Rate | ZAR : US$ | 10:1 | ||

Table 2: Production summary.

Key production totals are compared for each of the development scenarios.

| Production Summary | ||||

|---|---|---|---|---|

| Phase 1 4 Mtpa |

Phase 2 8 Mtpa(Base Case) |

Phase 3 12 Mtpa |

||

| Total Mined | Mt | 117 | 219 | 310 |

| Nickel | % | 0.34 | 0.35 | 0.34 |

| Platinum | g/t | 1.84 | 1.70 | 1.71 |

| Palladium | g/t | 1.93 | 1.78 | 1.77 |

| Copper | % | 0.16 | 0.16 | 0.16 |

| Gold | g/t | 0.27 | 0.27 | 0.27 |

| Rhodium | g/t | 0.13 | 0.12 | 0.12 |

| Recoveries (Life-of-Mine Average) | ||||

| Nickel Recovery | % | 69.13 | 69.47 | 69.05 |

| Platinum Recovery | % | 88.21 | 87.15 | 87.24 |

| Palladium Recovery | % | 87.63 | 86.85 | 86.77 |

| Copper Recovery | % | 87.89 | 87.90 | 87.84 |

| Gold Recovery | % | 76.69 | 76.72 | 76.72 |

| Rhodium Recovery | % | 85.92 | 86.62 | 86.62 |

| Concentrate Produced (Life-of-Mine Average Annual Production) | ||||

| Concentrate | ktpa | 156 | 292 | 413 |

| Nickel | % | 5.8 | 6.0 | 5.8 |

| Platinum | g/t | 40.50 | 37.04 | 37.30 |

| Palladium | g/t | 42.41 | 38.71 | 38.37 |

| Copper | % | 3.6 | 3.6 | 3.5 |

| Gold | g/t | 5.26 | 5.19 | 5.18 |

| Rhodium | g/t | 2.76 | 2.63 | 2.64 |

| 3PE+Au | g/t | 90.92 | 83.56 | 83.49 |

| Metal Sold (Life-of-Mine Average Annual Production Metal Units per Year) | ||||

| Nickel | Mlb | 20 | 39 | 53 |

| Platinum | koz | 203 | 348 | 495 |

| Palladium | koz | 212 | 364 | 510 |

| Copper | Mlb | 12 | 23 | 32 |

| Gold | koz | 26 | 49 | 69 |

| Rhodium | koz | 14 | 25 | 35 |

| 3PE+Au | koz | 455 | 785 | 1,109 |

Table 3: Pre-production capital cost.

The pre-production capital cost, including contingency, for each development scenario.

| US$M | Phase 1 4 Mtpa |

Phase 2 8 Mtpa (Base Case) |

Phase 3 12 Mtpa |

|---|---|---|---|

| Mining | |||

| Underground | 540 | 633 | 673 |

| Capitalized Pre-Production | 24 | 24 | 25 |

| Subtotal | 564 | 657 | 698 |

| Processing | |||

| Concentrator | 201 | 201 | 201 |

| Subtotal | 201 | 201 | 201 |

| Infrastructure | |||

| Bulk Water/Power | 76 | 76 | 76 |

| Tailings Dam | 39 | 46 | 39 |

| General Infrastructure | 29 | 29 | 29 |

| Subtotal | 144 | 151 | 144 |

| Indirects | |||

| Drilling & Studies | – | 19 | 19 |

| Mining: Indirects | 55 | 58 | 58 |

| Mining: EPCM | 80 | 93 | 97 |

| Processing & Infrastructure: EPCM | 37 | 37 | 37 |

| Subtotal | 172 | 207 | 211 |

| Owners Cost | |||

| Capitalized G&A | 26 | 26 | 26 |

| Mining | 60 | 79 | 79 |

| Processing & Infrastructure | 17 | 18 | 17 |

| Subtotal | 103 | 123 | 122 |

| Capital Expenditure Before Contingency | 1,185 | 1,338 | 1,376 |

| Mining Contingency | 221 | 259 | 272 |

| Processing & Infrastructure Contingency | 120 | 122 | 120 |

| Capital Expenditure After Contingency | 1,525 | 1,719 | 1,769 |

Table 4: Unit operating costs.

| $/oz Payable 3PE+Au | |||

|---|---|---|---|

| Phase 1 4 Mtpa |

Phase 2 8 Mtpa (Base Case) |

Phase 3 12 Mtpa |

|

| Mine-Site Cash Cost | 412 | 425 | 441 |

| Realization Cost | 402 | 416 | 413 |

| Total Cash Costs Before Credits | 814 | 840 | 854 |

| Nickel Credits | -367 | -411 | -397 |

| Copper Credits | -81 | -89 | -86 |

| Total Cash Costs After Credits | 367 | 341 | 371 |

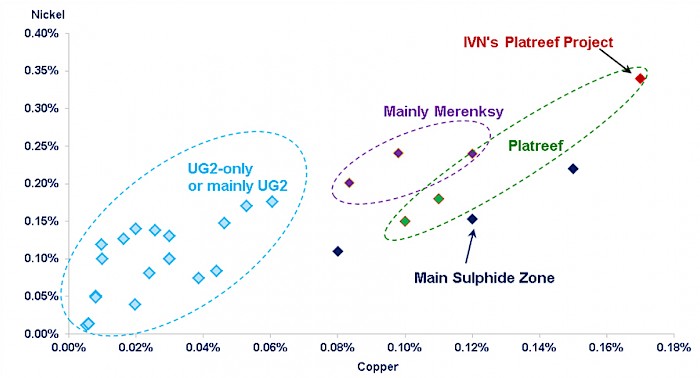

As illustrated in Figure 2, the Platreef Project has Africa’s highest concentration of copper and nickel among platinum-group metals (PGM) producers. UG2 ore bodies have relatively low by-products of nickel and copper to credit against operating costs, while the Merensky Reef and the main Sulphide Zone, in Zimbabwe, contain 0.10% to 0.25% nickel and 0.08% to 0.15% copper. The Platreef Project’s Indicated Mineral Resources (within the 2.0 g/t grade shell) contain 0.34% nickel and 0.17% copper.

The PEA includes an economic analysis that is based, in part, on Inferred Mineral Resources. Inferred Mineral Resources are considered too speculative geologically to have economic considerations applied to them that would allow them to be categorized as Mineral Reserves, and there is no certainty that the results will be realized. Mineral Resources are not Mineral Reserves because they do not have demonstrated economic viability.

Figure 2: Base-metal (nickel and copper) concentrations by PGM-bearing reef.

Source: SFA (Oxford). Data for Platreef Project and Waterberg are based on each project’s respective reported PEA parameters and are not representative of SFA’s view.

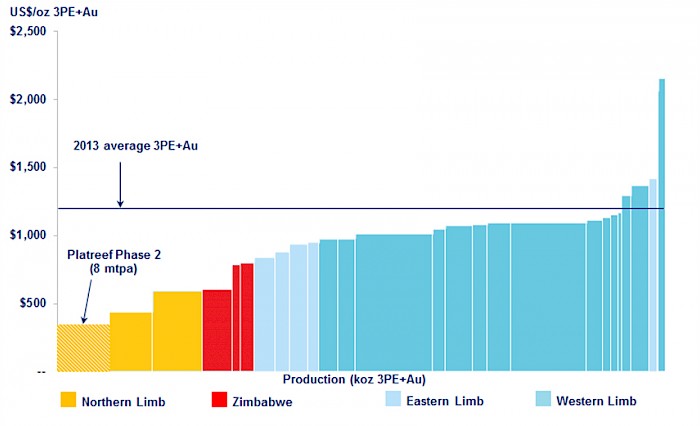

The higher nickel and copper grades contribute to lower operating cash costs for the Northern Limb as illustrated by Figure 3. Among the current and future Northern Limb producers, Platreef’s potential US$341 per 3PE+Au ounce, (net of base-metal by-products), ranks at the bottom of the cash-cost curve.

Figure 3: Net total cash cost (2013 mines in production and selected projects), US$/3PE+Au oz.

Source: SFA (Oxford). Data for Platreef Project and Waterberg are based on each project’s respective reported PEA parameters and are not representative of SFA’s view.

Pre-feasibility study and development of bulk-sample shaft under way

Surface construction work is underway for Shaft #1, the 7.25-metre-diameter bulk-sample shaft. The vertical shaft is planned to be sunk to a depth below surface of 800 metres and enable the collection of a mineralized bulk sample, expected in the first half of 2016, to complete the company’s development assessment of the Flatreef. South Africa-based Aveng Mining, the sinking contractor for Shaft #1, is continuing surface preparation work at the site; excavation of the box-cut access has begun. Upgrading of hoisting equipment to be installed in the shaft headframe is underway; excavations for concrete foundations of the shaft collar and ventilation casing are scheduled to begin this month.

Shaft #1, including some initial lateral, underground development work, is expected to be fully funded from dedicated funds remaining in Ivanhoe’s treasury from the US$280 million received in 2011 for the sale of an 8% interest in the Platreef Project to the Japanese consortium of Itochu Corporation; ITC Platinum, an Itochu affiliate; Japan Oil, Gas and Metals National Corporation; and Japan Gas Corporation.

Ivanhoe will begin the design and engineering of Shaft #2, the main production shaft, in Q2 2014. This will enable the company to start Shaft #2 development works in Q1 2015, subject to necessary approvals and funding.

A pre-feasibility study (PFS) also is underway and completion is targeted for the second half of 2014. The PFS currently focuses on the initial 4 Mtpa Phase 1 production case, based on selling or tolling concentrate at local smelters. Studies will continue on the base case 8 Mtpa Phase 2 and 12 Mtpa Phase 3 production scenarios with the intention of presenting an integrated development plan for the project incorporating the Phase 1 PFS.

Platreef ownership interests

Ivanhoe Mines holds an indirect 90% interest in the Platreef Project and the Itochu-led Japanese consortium holds the remaining 10% interest that it acquired in two investments made in 2010 and 2011.

In accordance with South African law, Ivanhoe Mines has proposed transferring a 26% interest in the Platreef Project to BBBEE SPV, a broad-based, black economic empowerment partner. Ivanhoe is discussing the required finalization of the BBBEE structure with the government’s Department of Mineral Resources, with a goal of securing the granting of the Platreef Mining Right by the department by the end of May this year. The proposed BBBEE, in which Ivanhoe would retain a 49% interest, would represent the interests of employees, as well as communities.

Upon receipt of the Mining Right, Ivanhoe will own 64% of the Platreef Project, BBBEE SPV will own 26% and the Japanese consortium will own 10%.

Mineral Resources characterized by large thicknesses

The Flatreef Mineral Resource, with a strike length of 6.5 kilometres, predominantly lies within a flat to gently-dipping portion of the Platreef mineralized belt that occurs at relatively shallow depths of approximately 700 to 1,100 metres below surface.

The Flatreef Deposit is characterized by its very large vertical thicknesses of high-grade mineralization and a platinum-to-palladium ratio of approximately 1:1, which is significantly higher than other recent PGM discoveries on the Bushveld’s Northern Limb. The 2.0 g/t 2PE+Au grade shells used to constrain mineralization in the Indicated Resource area within the Flatreef have average true thicknesses of approximately 24 metres, while the Indicated Mineral Resource grade at the equivalent 2.0 g/t 3PE+Au cut-off is 4.1 g/t platinum-palladium-gold-rhodium (3PE+Au), 0.34% nickel and 0.17% copper. Flatreef’s Indicated Mineral Resources of 214 million tonnes contain an estimated 28.5 million ounces of platinum, palladium, gold and rhodium, 1.6 billion pounds of nickel and 0.8 billion pounds of copper.

At the same cut-off of 2.0 g/t 3PE+Au, the current Flatreef estimate also includes Inferred Mineral Resources of 415 million tonnes grading 3.5 g/t 3PE+Au, 0.33% nickel and 0.16% copper, containing an estimated additional 47.2 million ounces of platinum, palladium, gold and rhodium, 3.0 billion pounds of nickel and 1.5 billion pounds of copper. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Details of the current Mineral Resource estimate, including a discussion of assumptions, parameters and methods, risks and uncertainties, individual metal grades and the relevant qualified persons, are set out in the Platreef Project NI 43-101 Technical Report on Updated Mineral Resource Estimate dated March 13, 2013, available on Ivanhoe Mines’ SEDAR profile at www.sedar.com and www.ivanhoemines.com.

Table 5: Mineral resources amenable to selective underground mining methods within and adjacent to the Turfspruit cyclic unit mineralized zone (based on resources reported to April 2013).

| Indicated Mineral Resources Tonnage and Grades |

||||||||

|---|---|---|---|---|---|---|---|---|

| Cut-off 3PE+Au | Mt | Platinum (g/t) |

Palladium (g/t) |

Gold (g/t) |

Rhodium (g/t) |

3PE+Au (g/t) |

Nickel (%) |

Copper (%) |

| 3 g/t | 137 | 2.27 | 2.31 | 0.35 | 0.15 | 5.09 | 0.38 | 0.18 |

| 2 g/t | 214 | 1.83 | 1.89 | 0.29 | 0.12 | 4.13 | 0.34 | 0.17 |

| 1 g/t | 387 | 1.28 | 1.34 | 0.21 | 0.09 | 2.92 | 0.28 | 0.14 |

| Contained Metal | ||||||||

| Cut-off 3PE+Au | – | Platinum (Moz) | Palladium (Moz) | Gold (Moz) | Rhodium (Moz) | 3PE+Au (Moz) |

Nickel (Mlbs) | Copper (Mlbs) |

| 3 g/t | – | 10.0 | 10.2 | 1.53 | 0.67 | 22.4 | 1,133 | 558 |

| 2 g/t | – | 12.6 | 13.0 | 2.00 | 0.85 | 28.5 | 1,610 | 794 |

| 1 g/t | – | 15.9 | 16.7 | 2.67 | 1.09 | 36.3 | 2,408 | 1,189 |

| Inferred Mineral Resources Tonnage and Grades |

||||||||

| Cut-off 3PE+Au | Mt | Platinum (g/t) |

Palladium (g/t) |

Gold (g/t) |

Rhodium (g/t) |

3PE+Au (g/t) |

Nickel (%) |

Copper (%) |

| 3 g/t | 211 | 2.09 | 2.06 | 0.34 | 0.14 | 4.63 | 0.38 | 0.18 |

| 2 g/t | 415 | 1.57 | 1.59 | 0.27 | 0.11 | 3.54 | 0.33 | 0.16 |

| 1 g/t | 1,054 | 0.96 | 1.02 | 0.18 | 0.07 | 2.23 | 0.26 | 0.13 |

| Contained Metal | ||||||||

| Cut-off 3PE+Au | – | Platinum (Moz) | Palladium (Moz) | Gold (Moz) | Rhodium (Moz) | 3PE+Au (Moz) | Nickel (Mlbs) | Copper (Mlbs) |

| 3 g/t | – | 14.2 | 14.0 | 2.29 | 0.97 | 31.5 | 1,764 | 855 |

| 2 g/t | – | 20.9 | 21.3 | 3.58 | 1.44 | 47.2 | 3,032 | 1,490 |

| 1 g/t | – | 32.7 | 34.7 | 5.95 | 2.32 | 75.7 | 5,934 | 3,035 |

Notes:

- Mineral Resources have an effective date of 3 April 2013. The Qualified Persons for the estimate are Dr. Harry Parker, RM SME, and Timothy Kuhl, RM SME.

- Mineral Resources estimated assuming underground selective mining methods within and adjacent to the TCU are exclusive of the Mineral Resources estimated assuming mass-mining methods.

- The 2.0 g/t 3PE+Au cut-off is considered the base-case estimate (highlighted); the 3.0 g/t 3PE+Au cut-off also is being considered.

- Mineral Resources are reported on a 100% basis. Mineral Resources are stated from approximately -200 m to 650 m elevation (from -500 m to 1,350 m depth). Indicated Mineral Resources are drilled on approximately 100 m x 100 m spacing; Inferred Mineral Resources are drilled on 400 m x 400 m (locally to 400 m x 200 m and 200 m x 200 m) spacing.

- Reasonable prospects for economic extraction were determined using the following assumptions. Assumed commodity prices are: nickel $8.81/lb; copper $2.73/lb; platinum $1,699/oz; palladium $667/oz; gold $1,315/oz; and rhodium $2,065/oz. It has been assumed that payable metals would be 82% from smelter/refinery and that mining costs (average $40/t) and process, G&A, and concentrate transport costs (average $12.50/t of mill feed for a 4 Mtpa operation) would be covered. The process recoveries vary with block grade but typically would be 85-90% for platinum, palladium and rhodium; 75% for gold; 70% for nickel; and 85% for copper.

- Totals may not sum due to rounding.

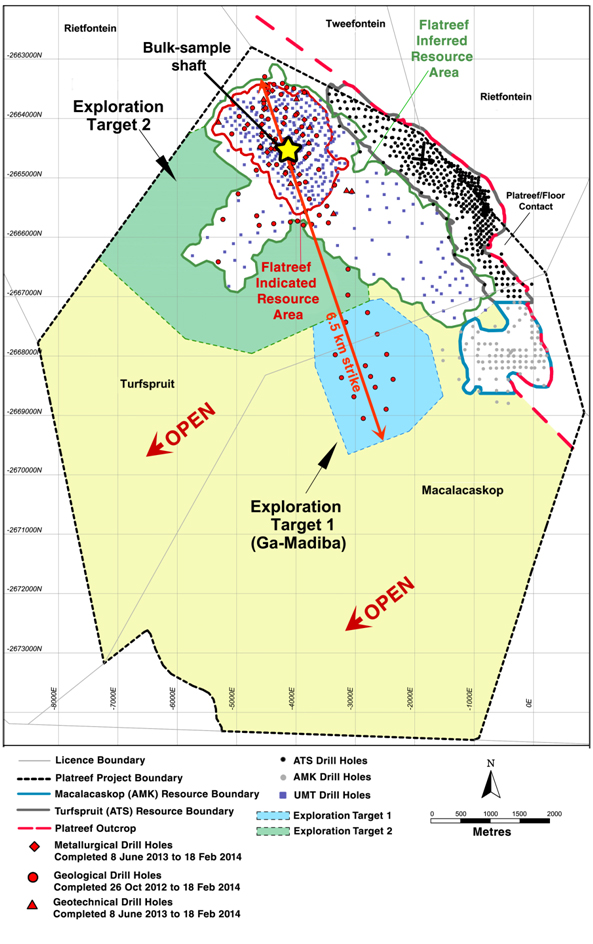

Indications of significant additional mineralization in adjacent exploration targets

As updated in Ivanhoe Mines’ recent news release issued on March 19, 2014, mineralization at the Platreef Project is open to expansion to the south and west, beyond the currently established Mineral Resources (see Figure 4). Two exploration targets have been identified.

Target 1, the Ga-Madiba extension zone, is based on results from 14 wide-spaced, step-out drill holes completed between October 26, 2012, and February 18, 2014. Ga-Madiba, which adjoins and stretches to the south from the area where Inferred Mineral Resources are estimated, could contain 115 to 235 million tonnes grading 3.1 to 4.5 g/t 3PE+Au (comprising 1.2 to 1.7 g/t platinum, 1.7 to 2.3 g/t palladium, 0.06 to 0.14 g/t rhodium, 0.17 to 0.26 g/t gold), 0.23% to 0.28% nickel and 0.11% to 0.14% copper over an area of 3.7 square kilometres. The tonnage and grade ranges are based on intersections of 2.0 g/t 3PE+Au mineralization in drill holes completed in Target 1.

Drilling to date has successfully identified the T1 and T2 mineralized reefs and confirmed the initial interpretation that the Ga-Madiba target represents the southern strike extension to the shallow-lying Flatreef. The overall drill results are encouraging and the depth, range of grade, thickness and grade-thickness are comparable to the initial, 400-metre-spaced drill results in Flatreef’s zone 1 (prior to completion of the 100-metre x 100-metre infill drill program).

Target 2, which surrounds the currently estimated mineral resources in zones 1 and 2, could contain an estimated 260 to 450 million tonnes grading 3.4 to 4.5 g/t 3PE+Au (comprising 1.7 to 2.4 g/t platinum, 1.2 to 1.6 g/t palladium, 0.14 to 0.20 g/t rhodium, 0.26 to 0.33 g/t gold), 0.30% to 0.35% nickel and 0.15% to 0.18% copper over an area of 7.6 square kilometres. The tonnage and grade ranges are based on 2.0 g/t 3PE+Au intersections of mineralization in 19 wide-spaced drill holes completed in Target 2 and adjacent drill holes within the Inferred Mineral Resource area. These drill holes were completed between October 26, 2012, and February 18, 2014.

Figure 4: Mineralization at the Platreef Project is open to expansion to the south and west, beyond the currently established Mineral Resources.

The potential quantity and grade of these exploration targets is conceptual in nature. There has been insufficient exploration and/or study to define these exploration targets as a Mineral Resource. It is uncertain if additional exploration will result in these exploration targets being delineated as a Mineral Resource. The potential quantity and grade of these exploration targets has not been used in the PEA.

In addition, there are approximately 37 square kilometres of unexplored ground beyond these two exploration target areas on the property under which the Platreef mineralization is projected to lie. It is not possible to estimate a range of tonnages and grades for this ground with current information. There is excellent potential for mineralization to significantly increase with further step-out drilling to the south-west.

Proposed mining methods

Stantec Consulting prepared an evaluation of three different production-rate scenarios (4 Mtpa, 8 Mtpa and 12 Mtpa) to mine the Indicated and Inferred Mineral Resources at the Platreef Project. The mining methods considered are long-hole stoping and drift-and-fill extraction, followed by either cemented paste, cemented rock fill or waste rock backfill, where applicable.

The mine plans have been developed for a total project life of 36 years, including a six-year pre production period prior to the mill start-up.

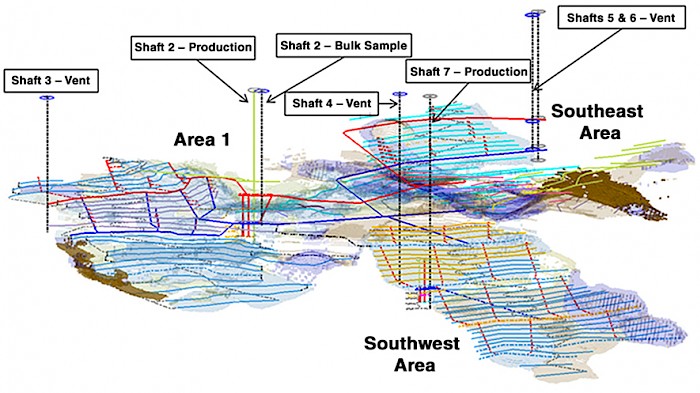

Figure 5: Mining areas and preliminary layouts for Phase 3 (12 Mtpa) development scenario (looking southeast).

Source: Stantec. Colours are for presentation only; they have no technical significance.

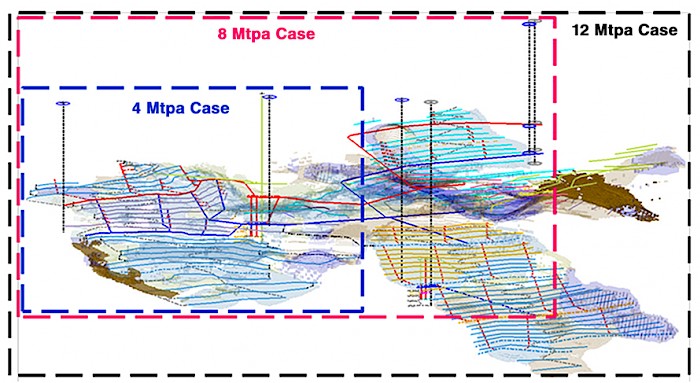

Figure 6: A similar view, to the southeast, illustrating the relative mine-expansion scenarios for Phase 1 (4 Mtpa), Phase 2 (8 Mtpa) and Phase 3 (12 Mtpa).

Source: Stantec. Colours are for presentation only; they have no technical significance.

Metallurgical test work and concentrator design

There have been a number of metallurgical test-work campaigns and conceptual flow-sheet designs carried out for the treatment of Platreef samples since 2001. Metallurgical test work focused on maximizing the recovery of platinum-group elements (PGEs) and base metals, mainly nickel, while producing an acceptably high-grade concentrate suitable for further processing and/or sale to a third party.

Previous comminution tests indicated that the plant feed is competent with respect to SAG milling and that a crusher and ball-mill circuit will be the preferred option. The Platreef material is classified as hard to very hard. The flotation test work has shown that the plant feed is amenable to treatment by conventional flotation without the need for re-grinding. Flotation losses from the circuit are due to a non-floating PGM population locked in gangue at sizes of 10 µm or finer.

Although this phase of the test work is preliminary, it did indicate that an effective flow sheet would involve several stages of cleaner flotation with recycling of the stage tailings. All of the three geo-met units and the two blends produced acceptable smelter-grade final concentrates at acceptable recoveries.

Based on the latest flotation test work results, a concentrator flow sheet was developed for the treatment of T1, T2 Upper and T2 Lower zones.

Phase 1 would include the construction of a 4 Mtpa concentrator and other associated infrastructure by 2020, in two modules of 2 Mtpa. Phase 2 would include a ramp-up to 8 Mtpa by 2024 and Phase 3 a further ramp-up to a plant capacity of 12 Mtpa by 2028.

A two-phased production approach was used for the Phase 1 flow-sheet development and design. The selected flow sheet is comprised of a common three-stage crushing circuit, feeding crushed material to two milling-flotation modules each of 2 Mtpa capacity. Milling is achieved in a ball mill with classification and rougher flotation in a split high-, medium- and low-grade circuit. Each concentrate is cleaned in a dedicated cleaner circuit with varying stages and recycles. Flotation is followed by tailings handling and concentrate thickening, filtration and storage.

Supply of electricity and water

The Olifants River Water Resource Development Project (ORWRDP) is designed to deliver water to the Eastern and Northern limbs of South Africa’s Bushveld Igneous Complex. The project consists of the new De Hoop Dam, the raising of the wall of the Flag Boshielo Dam and related pipeline infrastructure that ultimately will deliver water to Pruissen, southeast of Mokopane and the Platreef Project. The Pruissen Pipeline Project will be developed to deliver water on from Pruissen to the communities and mining projects on the Northern Limb. Ivanhoe is a member of the Joint Water Forum, which is part of the ORWRDP.

Participants in the water development scheme are required to indicate their water requirements so that total water demand may be calculated relative to the scheme’s capacity. These requirements are translated into a non-binding Memorandum of Agreement and then a binding, off-take agreement. The Platreef Project’s water requirement for the 8 Mtpa base case scenario would be approximately 22 million litres per day.

Eskom, the national power authority, has advised that sufficient power presently is not available in the Mokopane area due to transmission-line limitations and generating shortfalls. The generating shortfall should be alleviated with the first unit of the new Medupi Power Station that is due to begin operation in Q4 2014.

When fully operational, the Medupi Power Station will have the capacity to generate a total of up to 4,800 megawatts for the national grid.

The Medupi output, combined with the new Borutho main transmission substation, which is approximately 26 kilometres from the Platreef Project site and is due to begin operation this year, should ensure that sufficient power will be available for the Platreef Project.

Qualified persons, quality control and assurance

The following companies have undertaken work in preparation of the PEA:

- OreWin – Overall report preparation and financial model.

- AMEC – Mineral Resource estimation.

- SRK Consulting – Mine geotechnical recommendations.

- Stantec Consulting International – Underground mine plan.

- DRA – Process and infrastructure.

- Geo Tail – Tailings storage facility.

The independent qualified persons responsible for preparing the Platreef Preliminary Economic Assessment are Bernard Peters (OreWin); Dr. Harry Parker (AMEC); Timothy Kuhl (AMEC); William Joughin, (SRK); Mel Lawson (Stantec); Michael Valenta (Metallicon Process Consulting); and Guillaume de Swardt (Geo Tail).

The scientific and technical information in this news release has been reviewed and approved by Stephen Torr, P.Geo., Ivanhoe Mines’ Vice President, Project Geology and Evaluation, a Qualified Person under the terms of National Instrument 43-101. Mr. Torr has verified the technical data disclosed in this news release.

Base metals and other major-elements assays were determined by multi-acid digestion with ICP finish and PGEs were determined by conventional fire assay and ICP finish at Ultra Trace Geoanalytical Laboratories in Perth, Australia, an ISO 17025-accredited laboratory. Ivanhoe Mines utilized a well-documented system of inserting blanks and standards into the assay stream and has a strict chain of custody and independent laboratory re-check system for quality control.

Information on sample preparation, analyses and security is contained in the Platreef Project NI 43-101 Technical Report on Updated Mineral Resource Estimate dated March 13, 2013, filed on SEDAR at www.sedar.com and on the Ivanhoe Mines website at www.ivanhoemines.com.

Data verification

Dr. Parker and Mr. Kuhl, (collectively the AMEC QPs) reviewed the sample chain of custody, quality assurance and control procedures, and qualifications of analytical laboratories. The AMEC QPs are of the opinion that the procedures and QA/QC are acceptable to support Mineral Resource estimation. AMEC also audited the assay database, core logging and geological interpretations on a number of occasions between 2009 and 2013 and found no material issues with the data as a result of these audits.

In the opinion of the AMEC QPs, the data verification programs undertaken on the data collected from the Platreef Project support the geological interpretations, and the analytical and database quality and the data collected can support Mineral Resource estimation.

Details of the data verification supporting the Mineral Resource estimate are set out in the Platreef Project NI 43-101 Technical Report on Updated Mineral Resource Estimate dated March 13, 2013, available on Ivanhoe Mines’ SEDAR profile at www.sedar.com and www.ivanhoemines.com.

About Ivanhoe Mines

Ivanhoe Mines, with offices in Canada, the United Kingdom and South Africa, is advancing and developing its three principal projects:

- The Kamoa copper discovery in a previously unknown extension of the Central African Copperbelt in the DRC’s Province of Katanga.

- The Platreef Discovery of platinum, palladium, nickel, copper, gold and rhodium on the Northern Limb of the Bushveld Complex in South Africa.

- The historic, high-grade Kipushi zinc, copper and germanium mine, also on the Copperbelt in the DRC and now being upgraded to support a future return to production of copper, zinc and other metals following a care-and-maintenance program conducted between 1993 and 2011.

Ivanhoe Mines also is evaluating other opportunities as part of its objective to become a broadly based, international mining company.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.11.088.4300

Website www.ivanhoemines.com

FORWARD-LOOKING STATEMENTS

Statements in this release that are forward-looking statements are subject to various risks and uncertainties concerning the specific factors disclosed here and elsewhere in the company’s periodic filings with Canadian securities regulators. When used in this document, the words such as “could,” “plan,” “estimate,” “expect,” “intend,” “may,” “potential,” “should” and similar expressions, are forward-looking statements.

Among other items in this press release, all the results of the PEA represent forward-looking information. Specific statements in this release that constitute forward-looking statements or information include, but are not limited to: estimates of internal rates of return, net present value, future production from the Platreef Project (including the 4 Mpta, 8 Mpta and 12 Mpta production scenarios as well as the estimate of 785,000 ounces of future platinum, palladium, rhodium and gold (3PE+Au) production), estimates of cash cost (including the estimate of US$341 per ounce of 3PE+Au), proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, the grant of the Mining Right, future commodity price assumptions, estimates of capital costs, the completion of the sinking of Shaft #1 by the first half of 2016; the start of Shaft #2 development works in Q1 2015; the completion of the pre-feasibility study in the second half of 2014, and the availability and development of water and electricity projects (including the new De Hoop Dam) and the addition of the first unit of the new Medupi Power Station in Q4 2014. All other assumptions used in the PEA constitute forward-looking information.

Such forward-looking statements and information are based on certain assumptions and the opinions and estimates of management and qualified persons at the date the statements are made in light of their experience and perception of historical trends, current conditions and expected future developments, and are subject to a variety of risks and uncertainties and factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. The factors and assumptions used to develop the forward-looking information and statements, and the risks that could cause the actual results to differ materially are presented in the body of the Technical Report that will be filed on SEDAR at www.sedar.com and Ivanhoe Mines’ website at www.ivanhoemines.com within 45 days of this news release. In addition, these factors and assumptions include the grant of the Mining Right by end of May, 2014, the possibility of project cost overruns or unanticipated costs and expenses, the ability of contracted parties to perform as contracted, and that projects within the control of third parties (including power and water supplies) are developed and delivered as publically stated by such parties.

Forward-looking statements and information are also subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information or statements. Important other factors that could cause actual results to differ from these forward-looking statements include those described under the heading “Risk Factors” in the company’s most recently filed MD&A and Annual Information Form. Readers are cautioned not to place undue reliance on forward-looking information or statements. The Company undertakes no obligation to update any forward-looking information or statements except as required by law.