English

English Français

Français 日本語

日本語 中文

中文TORONTO, CANADA – Ivanhoe Mines (TSX: IVN) today announced its financial results for the first quarter ended March 31, 2014. All figures are in U.S. dollars unless otherwise stated.

HIGHLIGHTS

- Ivanhoe Mines initiated its 20,000-metre underground drilling program at the Kipushi zinc-copper mine in the Democratic Republic of Congo in March 2014. The drilling is designed to confirm and update Kipushi’s estimated historical resources and to further expand the resources on strike and at depth. Drilling to date has totalled approximately 2,800 metres. Early drilling intersected zones of significant copper mineralization (chalcopyrite and bornite) and zinc mineralization (sphalerite), extending mineralization in the Big Zinc Discovery to a depth of approximately 1,700 metres below surface, 200 metres deeper than the previous lowest level of the historical Measured and Indicated Resources. Assays are pending.

- In March 2014, Ivanhoe announced that an independent review of core from previous holes drilled by state-owned Gécamines in the early 1990s into Kipushi’s Big Zinc Discovery indicated that tonnage and grade of the Big Zinc had been understated in a historical estimate. The review concluded that the new assays averaged 5.5% higher than results originally reported by Gécamines and that density applied by Gécamines for estimating the tonnage in the Big Zinc was understated by an average of 9%.

- On March 26, 2014, Ivanhoe welcomed the positive findings of an independent, preliminary economic assessment (PEA) of its Platreef platinum-palladium-gold-nickel-copper project in South Africa. The PEA estimated that at the planned, base-case mining rate of eight million tonnes per year the mine would become Africa’s lowest-cost producer of platinum-group metals, with annual production of 785,000 ounces of platinum, palladium, rhodium and gold. Ivanhoe is awaiting the grant of a Mining Right for the Platreef Project that would permit the company to mine and process minerals from the mining area for a period of 30 years, and which may be extended upon application.

- In March 2014, Ivanhoe Mines signed a financing agreement with D.R. Congo’s La Société Nationale d’Electricité (SNEL), allowing the rehabilitation of existing hydroelectric power plants. Completion of the work would entitle Ivanhoe to receive a combined total of 200 megawatts from the national power grid, ensuring sufficient power for the planned 300,000-tonne-per-year smelter and the associated future mine expansions at Ivanhoe’s Kamoa copper development project.

- On May 6, 2014, Ivanhoe Mines announced the appointment of senior South African mining executive Mark Farren as the company’s Executive Vice President of Operations, to take effect in mid-June. Mr. Farren will assume lead responsibilities for the various engineering and development activities now underway as Ivanhoe Mines continues to advance its three principal projects in Sub-Saharan Africa.

- Also in May, Ivanhoe Mines reported in a news release that ongoing exploration and development work at the company’s Kamoa copper project in D.R. Congo had further confirmed that the focus of the company’s initial mine development at Kamoa would be on the high-grade Kansoko Sud area, where infill drilling since the last resource estimate was produced in 2012 has defined a thick, near-surface zone of high-grade copper sulphide mineralization that would be amenable to treatment by a conventional copper flotation plant.

Principal Projects and Review of Activities

Ivanhoe Mines, with offices in Canada, the United Kingdom and South Africa, is developing its three principal projects:

- The Kamoa copper discovery in a previously unknown extension of the Central African Copperbelt in the DRC’s Province of Katanga.

- The Platreef discovery of platinum, palladium, nickel, copper, gold and rhodium on the Northern Limb of the Bushveld Complex in South Africa.

- The historic, high-grade Kipushi zinc, copper and germanium mine, also on the Copperbelt in the DRC, now being drilled and upgraded following an 18-year care-and-maintenance program that ended when Ivanhoe acquired its majority interest in the mine in 2011.

Ivanhoe is evaluating other opportunities as part of its objective to become a broadly based, international mining company.

1. Kamoa Project

95%-owned by Ivanhoe Mines

Democratic Republic of Congo (DRC)

An updated preliminary economic assessment (PEA) was published in November 2013 that reflects a phased approach to development of the Kamoa Project. The first phase of mining would target high-grade copper mineralization from shallow, underground resources to yield a high-value concentrate. The second phase would entail a major expansion of the mine and mill and construction of a smelter to produce blister copper.

Highlights of the Kamoa PEA

- A large mine and smelter would be developed using a two-phased approach.

- A smaller-scale start-up would establish an operating platform to support expansion.

- Early cash flows would be generated from the sale of high-grade copper concentrate.

- Low pre-production capital requirement of approximately $1.4 billion.

- Steady-state production target of 300,000 tonnes per year of blister copper, which would establish Kamoa as one of the world’s largest copper mines, with the highest grade.

- Cash costs of $1.19 per pound of copper would rank Kamoa near the bottom of the global cash-cost curve.

- $2.6 billion after-tax net present value, at an 8% discount rate.

- 15.3% after-tax internal rate of return.

The initial mining rate and concentrate feed capacity of three million tonnes per year would be followed in Year 5 by an additional expansion of eight million tonnes per year in concentrator capacity and the construction of an on-site smelter with a capacity to produce 300,000 tonnes per year of blister copper. In addition, an estimated 1,600 tonnes of sulphuric acid per day would be produced as a by-product of the copper smelting process. The PEA contemplates that the sulphuric acid would be sold to copper-oxide mining operations on the Central African Copperbelt that presently purchase acid from Zambia or from overseas.

The production scenario projects that 326 million tonnes would be mined and milled at an average copper grade of 3.0% copper over a 30-year mine life, producing 7.8 million tonnes of payable blister copper (plus 0.5 million tonnes of payable copper in concentrate in the initial concentrate phase) over the life of the project.

Steady-state production from Year 6 onward of 306,000 tonnes per year of blister copper would establish Kamoa as one of the world’s largest copper mines. Kamoa also would have the highest average grade among the 20 largest copper mines currently in production, or expected to be in production, according to data from Wood Mackenzie, an international industry research and consulting group.

Initial mine economics should benefit from narrower, higher-grade intervals

Infill drilling of Kamoa’s primary mining targets has confirmed the overall grade and thickness of the December 2012 resource estimate in these areas and provided invaluable refinement within localized areas. While traditionally modelled on a 1% total copper cut-off to define a selective mineralized zone, the deposit has shown that grade continuity also exists at an elevated 1.5% total copper vertical cut-off, and that a 2.0% vertical total copper cut-off may be feasible in certain areas.

Recent work defining the selective mineralized zone (SMZ) at higher vertical cut-offs has shown that narrower, higher-grade intervals create more expansive, contiguous zones, which should improve initial mine economics.

A new base case for future engineering studies is being developed using a 1.5% total copper cut-off with a minimum three-metre mining height and a maximum mining constraint of six metres (a single mining cut); incremental mineralization above six metres will be included only if the grade of the incremental mineralization exceeds 2%. This approach was introduced for thicker intercepts, to ensure initial mining cuts would extract only higher-grade material.

Progress on pre-feasibility study, with initial mining at Kansoko Sud

In line with the phased approach to project development outlined in the 2013 updated Kamoa PEA, the Kamoa pre-feasibility study (PFS) is progressing on the basis of an initial three-million-tonne-per-annum (3Mtpa) mine and concentrator.

The focus in planning the early years of mine production continues to be on the near-surface and high-grade material from the Kansoko Sud area to maximize margins. The 3Mpta mine and concentrator can be split into modules to potentially better match the underground ramp-up and further reduce the pre-production development capital. This will be examined in more detail as part of the pre-feasibility study to provide flexibility to the development of the Kamoa Project.

Preparations are underway to start the first mine-access decline at Kansoko Sud. The decline is designed to provide access to the high-grade copper resources that would be targeted for the planned first phase of production using the room-and-pillar mining method.

A pre-feasibility-level development study is underway to advance the geotechnical, engineering and metallurgical understanding of Kamoa. Phase 6 of the metallurgical testwork program is being conducted at the XPS laboratories in Sudbury, Canada, and the Mintek laboratories in Johannesburg, South Africa. Phase 6A testwork considers the first four years of mining, during which flotation concentrate will be sold. The phase 6B testwork considers the next 15 years of mining, from year five onward, when blister copper would be produced. This work is expected to be completed in Q2 2014.

Exploration drilling during the first quarter of 2014 was focused on resource infill, metallurgical studies and exploration drilling. Six drill rigs were in operation, including two truck-mounted rigs owned by Ivanhoe. Forty-five holes totalling 9,315 metres were completed during the quarter; comprised of 6,474 metres for resource evaluation and variability, 2,120 metres for metallurgical testing in the Kamoa Sud, Kansoko Central, Kansoko Sud and Makalu areas, and 721 metres of exploration drilling in the Kansoko East area.

Planned additional drilling in 2014

Planned drilling for the remainder of 2014 will target an initial, high-grade development area in Kansoko Sud, as well as some early-stage exploration drilling in the Kakula area south of the currently defined Kamoa Project resources.

Agreement signed to upgrade existing hydroelectric power plants

In March 2014, a financing agreement was signed between Ivanhoe and the DRC’s national electricity company, La Société Nationale d’Electricité (SNEL). Ivanhoe is working with SNEL to upgrade two existing hydroelectric power plants — Mwadingusha and Koni — to recover up to 113 megawatts of capacity to be made available to the national power supply grid. SNEL will provide the Kamoa Project with up to 100 megawatts from the grid, which would be sufficient to operate the initial phase of the Kamoa mine.

A third hydroelectric power plant — Nzilo 1 — would follow under the same financing agreement. Nzilo 1 will have a capacity of approximately 108 megawatts upon completion, entitling Kamoa to receive an additional 100 megawatts from the grid. The upgraded technology planned to be applied will increase the original design capacity of these power plants by up to 10%.

A combined total of 200 megawatts from the grid would provide sufficient power for Kamoa’s 300,000 tonnes per year smelter and the associated future mine expansions.

2. Platreef Project

90%-owned by Ivanhoe Mines

South Africa

The Platreef Project, in South Africa’s Limpopo province, is 90%-owned by Ivanhoe and 10%-owned by a Japanese consortium of Itochu Corporation; ITC Platinum, an Itochu affiliate; Japan Oil, Gas and Metals National Corporation; and Japan Gas Corporation. The Japanese consortium’s 10% interest in the Platreef Project was acquired in two tranches for a total investment of $290 million.

The Platreef Project includes the underground Flatreef Deposit of thick, platinum-group elements, nickel, copper and gold mineralization in the Northern Limb of the Bushveld Complex, approximately 280 kilometres northeast of Johannesburg.

Platreef also planning a phased approach to a large, mechanized mine

An independent preliminary economic assessment was released in March 2014 that reflects a phased approach to development of the Platreef Project. Initiating production with a four-million-tonne per year first phase would establish an operating platform to support future expansions. Subsequent phases would see production expanded to eight million tonnes per year, and then to 12 million tonnes per year.

Highlights of the Platreef PEA

- A large, mechanized, underground mine is planned to be developed through a phased approach.

- Three run-of-mine production scenarios were examined: 4 million tonnes per year (Mtpa); a base case of 8 Mtpa; and 12 Mtpa.

- An initial 4 Mtpa scenario would establish an operating platform.

- Expansions — to the base-case 8 Mtpa scenario, and also to the 12 Mtpa scenario — could be accelerated as the market dictates.

- Opportunities exist for additional phases of development beyond 12 Mtpa, subject to further study.

Key features of the 8 million tonnes/year base-case scenario

- Annual production target of 785,000 ounces of platinum, palladium, rhodium and gold. (At an expanded operating scenario of 12 million tonnes per year, the annual production target would be 1.1 million ounces of platinum, palladium, rhodium and gold (3PE+Au)).

- Platreef, with the highest concentration of base metals among Africa’s producers of platinum-group metals, would rank at the bottom of the cash-cost curve, at an estimated $341 per ounce of 3PE+Au, net of by-products.

- Estimated pre-production capital requirement of approximately $1.7 billion, including $381 million in contingencies.

- $1.6 billion after-tax net present value, at an 8% discount rate.

- 14.3% after-tax internal rate of return.

The base case for the Platreef PEA analysis is the 8 Mtpa production scenario. The scenarios describe a staged approach, where there would be opportunity to expand the operation depending on demand, smelting and refining capacity and capital availability. As the 4 Mtpa production scenario (Phase 1) is developed and placed into production, there is opportunity to modify and optimize the subsequent phases, allowing for changes to the timing or expansion capacity to suit the conditions at the time. Opportunities for additional expansion beyond 12 Mtpa (Phase 3) may be available, but require additional investigation.

Phase 1 would include the construction of a concentrator and other associated infrastructure to establish an operating platform to support the start of production at a nominal plant capacity of 4 Mtpa by 2020. Phase 2 would include a ramp-up to a plant capacity of 8 Mtpa by 2024; Phase 3 envisages a further ramp-up to a steady-state plant capacity of 12 Mtpa by 2028.

The Platreef preliminary economic assessment technical report has been filed on SEDAR at www.sedar.com and on the Ivanhoe Mines website at www.ivanhoemines.com.

Mining Right approval pending

A Mining Right Application (MRA) for the Platreef Project was filed with the South African government’s Department of Mineral Resources (DMR) in June 2013. It would permit the company to mine and process minerals from the mining area for a period of 30 years, which may be extended upon application.

The application review process involves a thorough assessment of Ivanhoe’s Environmental Management Program, Social and Labour Plan, Mining Works Program and Broad-Based Black Economic Empowerment structure. The entire application process is being administered by the DMR. Ivanhoe recently amended its proposed BBBEE structure. It now includes communities, employees and entrepreneurs, who together will own 26% of the Platreef Project. Ivanhoe has received feedback from the DMR on the various aspects of its application and expects to receive approval of its Mining Right shortly. However, this may not occur prior to the expiry of the company’s prospecting right on May 31, 2014.

Based on legal consultation, it has been established that if Ivanhoe does not receive the Mining Right by May 31, 2014, the company’s prospecting right would expire and the company would be required to suspend all physical exploration activities on the Platreef Project, including work on the bulk-sample shaft, until the Mining Right is granted by the DMR. However, expiry of the prospecting right would not impact on the exclusivity Ivanhoe enjoys with regard to the mining right application, which prevents any other party from applying for a right over the same area.

Development of bulk-sample shaft proceeding

Surface construction work is underway for Shaft #1, the 7.25-metre-diameter bulk-sample shaft. The vertical shaft is planned to be sunk to a depth below surface of 800 metres and enable the collection of a mineralized bulk sample, expected in the first half of 2016, to complete the company’s development assessment of the Flatreef. South Africa-based Aveng Mining, the shaft-sinking contractor, is continuing the excavation of the box-cut access for the shaft collar and vent plenum. Upgrading of hoisting equipment, to be installed in the shaft headframe, also is underway.

Shaft #1, including some initial lateral, underground development work, is expected to be fully funded from dedicated funds remaining in Ivanhoe’s treasury from the US$280 million received in 2011 for the sale of an 8% interest in the Platreef Project to the Itochu-led Japanese consortium.

Ivanhoe will begin the design and engineering of Shaft #2, the main production shaft, in Q2 2014. This will enable the company to start Shaft #2 development works in Q1 2015, subject to necessary approvals and funding.

Completion of a pre-feasibility study (PFS) — currently focused on the Phase 1, 4 Mtpa production case, based on selling or tolling concentrate at local smelters — is targeted for the second half of 2014. Studies will continue on the Phase 2, base case 8 Mtpa and Phase 3, 12 Mtpa production scenarios, with the intention of presenting an integrated development plan for the project that would incorporate the Phase 1 PFS.

Exploration and development drilling

Ivanhoe plans to complete 90,000 metres of diamond drilling as part of its 2014 exploration and expansion program focused on four areas: Northern Zone 1, Zone 3, Zone 2 and the Ga-Madiba 400-metre grid. The goal is to delineate additional Indicated Mineral Resources in the immediate vicinity of Zone 1 that would support an eight-million-tonne-per-year (phase 2) pre-feasibility study and also allow for the potential declaration of an initial Inferred Mineral Resource estimate on the Ga-Madiba extension zone.

Thirty-six holes totalling 27,530 metres were drilled during Q1 2014, including nine deflections. Metallurgical bulk sampling and comminution drilling accounted for 4,464 metres in seven holes. Twenty-nine exploration holes drilled during the quarter totalled 23,065 metres, focused on Northern Zone 1, delineating the extension of the Bikurri Reef and extending defined mineralization on the T1 and T2 reefs, on the western extension of the Flatreef, and into Zone 3.

Drilling has been completed for metallurgical samples for variability and mini-pilot-plant testwork. Variability testwork is expected to start during Q2 2014, followed by work on the mini pilot plant.

3. Kipushi Project

68%-owned by Ivanhoe Mines

Democratic Republic of Congo (DRC)

The Kipushi copper-zinc-germanium-lead mine, in southern Katanga Province, is adjacent to the town of Kipushi and approximately 30 kilometres southwest of the provincial capital of Lubumbashi. It also is on the Central African Copperbelt, southeast of the company’s Kamoa Project, and less than one kilometre from the Zambian border. Ivanhoe acquired its 68% interest in the Kipushi Project in November 2011; the balance of 32% is held by La Générale des Carrières et des Mines (Gécamines), the DRC’s state-owned mining company.

Project development and infrastructure

Work began in early March 2014 on the planned diamond-drilling program at the Kipushi Project, a major advance made possible by the ongoing dewatering program directed by Ivanhoe during the past two and a half years following its acquisition of a 68% interest in Kipushi in November 2011.

The mine, which had been placed on care and maintenance in 1993, flooded in early 2011 due to a lack of pump maintenance over an extended period. Water reached 851 metres below surface at its peak. A major milestone was reached in December 2013 when Ivanhoe restored access to the mine’s principal haulage level at 1,150 metres below the surface.

Since gaining access to the 1,150-metre level in December, crews have been upgrading underground and surface infrastructure to support the drilling program. Two rigs have been conducting underground drilling at the mine, de-watering is ongoing and access to the important 1,272-metre-level hanging-wall drift is expected by the end of the second quarter of 2014, which will allow Ivanhoe to begin the drill program’s phase of twinning the historical drilling.

The next stage of the dewatering program is to replace the winding ropes on the Shaft 5 conveyances and re-establish the main pumping station in Shaft 5 at the 1,210-metre level for ongoing dewatering.

Exploration and development drilling

Ivanhoe’s 2014 underground drilling program is scheduled to complete approximately 100 holes totalling more than 20,000 metres. The drilling program is designed to confirm and update Kipushi’s estimated historical resources and to further expand the resources on strike and at depth. Drilling to date has completed approximately 2,800 metres.

Summary of initial drilling highlights previously released

- Hole KPU001, drilled at -67 degrees on a bearing of 298 degrees, drilled through massive sphalerite and dolomite from 46.4 metres to 399.36 metres. This approximately 353-metre intersection extends to a depth below surface of 1,550 metres.

- Hole KPU002, drilled on the same azimuth as KPU001 but at an inclination of -61 degrees, also intersected the Big Zinc from 32.05 metres to 372.4 metres (total intersection length of approximately 340 metres), to a depth of 1,590 metres below surface.

- Hole KPU003, drilled on a bearing of 273 degrees, aimed to test the southern plunge of the Big Zinc. This hole successfully intersected massive sphalerite and dolomite from 31 metres to a drilled depth of 550 metres down-hole, or 1,700 metres below surface. Importantly, the hole also intersected significant copper mineralization (chalcopyrite and bornite) from 194.4 metres to 225 metres down hole and a breccia-hosted zone of copper mineralization (chalcopyrite) from 439 metres to 461.6 metres.

- Hole KPU004, drilled from the 1,251-metre level on a bearing of 005 degrees and inclination of -45 degrees, intersected zones of chalcopyrite in the Série Récurrente mineralized zone, part of the historically mined North Orebody, from 56.5 metres to 71.5 metres, including massive chalcopyrite from 58.4 metres to 59.4 metres and 60.0 metres to 62.1 metres.

Ivanhoe’s current exploration at Kipushi has been focusing on drilling copper zones in the Série Récurrente zone from the drill station at the 1,251-metre level, from which KPU004 was drilled, and also on drilling holes to understand the stratigraphic succession. Drilling at the 1,251-metre level has continued to show encouraging results and the initial program in this area has been expanded. The zone being targeted by the expanded drill program lies below and to the east of the historical measured and indicated resources of the Série Récurrente.

Core from Hole KPU003 showing massive orange sphalerite and pyrite in the Big Zinc.

Core from KPU004, the first hole drilled in the Série Récurrente zone on Kipushi’s northern limb, which intersected a 15-metre, copper-rich mineralized zone.

Ivanhoe cautions that the presence of mineralization observed in the drilling to date at Kipushi is not presented to confirm historical assay results. It confirms only the presence of mineralization similar in style to that observed in historical holes drilled by state-owned mining company, Gécamines. Assays for copper, zinc, lead, germanium and precious metals are pending.

Big Zinc’s grade and tonnage potentially are higher than previously estimated, new review indicates

Ivanhoe recently received the findings of an independent review conducted by MSA Group (Pty.) Ltd., of Johannesburg, based on results of a comprehensive re-sampling program of historical Kipushi core collected from drilling by Gécamines into the Big Zinc Discovery in the early 1990s.

A total of 384 historical quarter-core (NQ-sized) samples were collected and dispatched to Bureau Veritas Minerals Pty. Ltd.’s laboratory in Australia. A total of 457 samples, including quality-control samples, were submitted to Bureau Veritas and analyzed for gold by fire assay, and for multi-elements, including zinc and copper, by sodium peroxide fusion and ICP-AES/MS finish. The re-sampling program was conducted over eight complete drill intersections of the Big Zinc from eight separate section lines and represented 18% of the total samples in the Big Zinc’s historical assay database.

MSA’s review of the recent re-sampling revealed that the zinc assay results generally report higher — and averaged 5.5% higher — than the assay results originally reported by Gécamines. MSA also concluded that density applied by Gécamines for estimating the tonnage in the Big Zinc Discovery was understated by an average of 9%. Despite the low bias, the review confirms that historical assay values reported by Gécamines are reasonable and can be replicated within a reasonable level of error by international, accredited laboratories under strict QA/QC control. This is an important milestone for Ivanhoe as part of its program to establish current resource estimates for its Kipushi Project.

Senior South African mining executive Mark Farren to join Ivanhoe Mines as head of operations

On May 5, 2014, Ivanhoe Mines announced the appointment of Mark Farren as the company’s Executive Vice President of Operations, effective June 15, 2014. He will assume lead responsibilities for the various engineering and development activities at the Kamoa, Kipushi and Platreef projects.

Mr. Farren also will assume principal duties presently performed by Ivanhoe’s Chief Operating Officer Michael Gray, who will retire from his day-to-day role with Ivanhoe at the end of June. Mr. Gray will continue to advise the company on mining related matters as a consultant.

Executive Vice President and Chief Development Officer Steve Garcia, who helped establish the foundations for Ivanhoe’s corporate growth and project development, resigned from the company at the end of April, 2014.

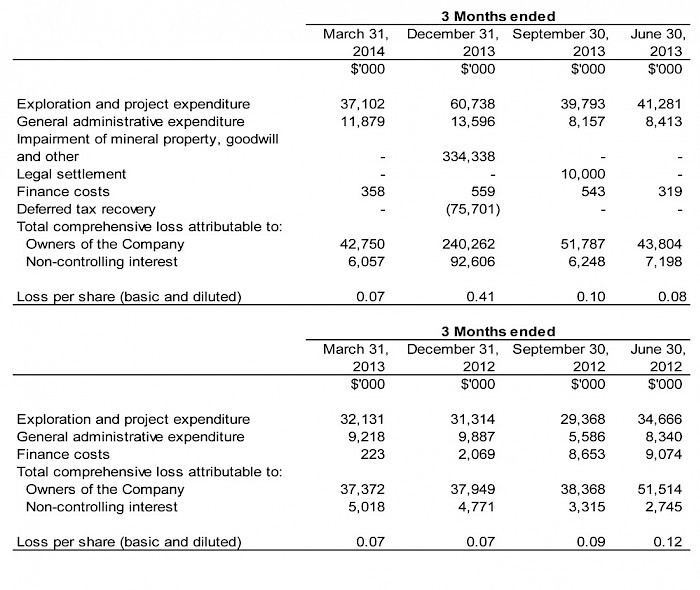

SELECTED QUARTERLY FINANCIAL INFORMATION

The following table summarizes selected financial information for the prior eight quarters. Other than its share of revenue from the RK1 Consortium, Ivanhoe had no operating revenue in any financial reporting period and did not declare or pay any dividend or distribution in any financial reporting period.

Review of the Three Months ended March 31, 2014, vs. March 31, 2013

The company’s total comprehensive loss for Q1 2014 of $48.8 million was $6.4 million higher than for the same period in 2013 ($42.4 million). The increase mainly was due to an increase in exploration and project expenditures of $5.0 million and an increase in foreign exchange losses of $2.1 million due to the weakening of the Canadian Dollar against the United States Dollar.

Exploration and project expenditures for the three months ending March 31, 2014, were $5.0 million higher than for the same period in 2013. This mainly was due to increases in expenditure of $5.9 million at the Platreef Project.

Financial position as at March 31, 2014, vs. December 31, 2013

The company’s total assets decreased to $238.9 million as at March 31, 2014, from $287.6 million as at December 31, 2013. This mainly was due to a $53.9 million decrease in cash and cash equivalents.

The company utilized $44.9 million of its cash resources in its operations and earned interest income of $0.3 million on cash balances. A total of $7.5 million was spent to acquire property, plant and equipment and other non-current assets.

Of the $7.5 million spent to acquire non-current assets, $2.4 million related to initial costs to secure electricity for the Platreef Project, while $3.0 million related to the cost incurred on the Platreef bulk-sample shaft during Q1. The remainder of the additions to property, plant and equipment mainly related to the procurement of assets required at the other projects.

The company’s total liabilities decreased from $60.3 million as at December 31, 2013, to $57.8 million as at March 31, 2014. This mainly was due to a decrease in trade and other payables of $2.9 million.

Liquidity and capital resources

Ivanhoe Mines had $89.9 million in cash and cash equivalents and $80.3 million in short-term deposits as at March 31, 2014. Certain of the company’s cash and cash equivalents and short-term deposits, having an aggregate value of $146.7 million, are subject to contractual restrictions as to their use and are reserved for the Platreef Project. Based on current planned work programs, these restricted funds should be sufficient to advance the Platreef Project until early 2015.

As at March 31, 2014, the company had consolidated working capital of approximately $149.8 million, compared to $201.7 million at December 31, 2013. The Platreef Project working capital is restricted and amounted to $145.2 million at March 31, 2014, and $161.6 million at December 31, 2013. Excluding the Platreef Project working capital, the resultant working capital was $4.6 million at March 31, 2014, and $40.1 million at December 31, 2013. Any future working capital deficiency is expected to be remedied through a debt or equity financing. The company’s access to financing is always uncertain and there can be no assurance that additional funding will be available to the company in the near future.

The company’s main objectives for 2014 remain the Bulk Sample Shaft development at the Platreef Project, which will be funded from the restricted funds available to Platreef only, the commencement of the underground mine-access decline at the Kamoa Project and the underground drilling program at the Kipushi Project. However, the company does not have sufficient funds to meet these objectives at Kamoa or Kipushi without further funding by the end of Q2 2014.

Corporate and project-level options being evaluated

In order to help realize the potential value of its world-scale mineral projects in Africa for all of its stakeholders, Ivanhoe Mines also has commenced an examination of a number of potentially significant corporate and project-level options. These include a corporate reorganization; project spin-offs (including potentially separating its South African platinum assets and its DRC copper and zinc assets into separately listed public companies); sales or joint ventures; project- or corporate-level debt and/or equity investments (including interim financing); and additional and/or alternative stock-exchange listings for certain of the company’s projects. While the company has started examining the commercial viability of some of these options, further detailed structuring and study of tax, legal, and operational costs and effects remain to be completed. The company also continues to progress ongoing discussions and negotiations with third-party strategic investors and joint-venture parties.

This release should be read in conjunction with Ivanhoe Mines’ unaudited Q1’14 Financial Statements and Management’s Discussion and Analysis report available at www.ivanhoemines.com and at www.sedar.com.

Qualified Person

Disclosures of a scientific or technical nature in this news release have been reviewed and approved by Stephen Torr, who is considered, by virtue of his education, experience and professional association, a Qualified Person under the terms of National Instrument 43-101. Ivanhoe Mines has prepared a NI 43-101-compliant technical report for each of the Kamoa Project, the Platreef Project and the Kipushi Project, which are available at www.sedar.com. These technical reports include relevant information regarding the effective date and the assumptions, parameters and methods of the mineral resource estimates on the Kamoa Project and Platreef Project cited in this news release, as well as information regarding data verification, exploration procedures and other matters relevant to the scientific and technical disclosure contained in this news release in respect of the Kamoa Project, Platreef Project and Kipushi Project.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.11.088.4300

Website www.ivanhoemines.com

Cautionary statement on forward-looking information

Certain statements in this release constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws, including without limitation, the timing and results of: (i) a development study at the Kamoa Project which contemplates the declaration of a mineral reserve estimate (“Development Study”); (ii) plans to start the first underground mine-access decline at the Kamoa Project in 2014; (iii) a grant of a mining right for the Platreef Project by May 2014; (iv) the creation of a Broad-Based Black Economic Empowerment structure for the Platreef Project; (v) the completion of a pre-feasibility study (“PFS”) at the Platreef Project by the second half of 2014; (vi) the commencement of the design and engineering of the main production shaft (Shaft #2) at the Platreef Project in Q2 2014; (vii) the collection of a mineralized bulk sample at the Platreef Project by the first half of 2016 (viii) plans to start Shaft #2 development works in Q1 2015; (ix) efforts to upgrade historical resource estimates at the Kipushi Project; and (x) the de-watering program at the Kipushi Project. Such statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as “may”, “would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate”, “scheduled”, “forecast”, “predict” and other similar terminology, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. These statements reflect the company’s current expectations regarding future events, performance and results and speak only as of the date of this release.

As well, the results of the preliminary economic assessments of the Kamoa Project and the Platreef Project constitute forward-looking information, including estimates of internal rates of return, net present value, future production, estimates of cash cost, proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, and estimates of capital and operating costs. Furthermore, with respect to this specific forward looking information concerning the development of the Kamoa and Platreef Projects, the company has based its assumptions and analysis on certain factors which are inherently uncertain. Uncertainties include among others: (i) the adequacy of infrastructure; (ii) geological characteristics; (iii) metallurgical characteristics of the mineralization; (iv) the ability to develop adequate processing capacity; (v) the price of copper, nickel, platinum, palladium, rhodium and gold; (vi) the availability of equipment and facilities necessary to complete development, (vii) the cost of consumables and mining and processing equipment; (viii) unforeseen technological and engineering problems; (ix) accidents or acts of sabotage or terrorism; (x) currency fluctuations; (xi) changes in regulations; (xii) the availability and productivity of skilled labour; (xiii) the regulation of the mining industry by various governmental agencies; and (xiv) political factors.

This release also contains references to estimates of Mineral Resources. The estimation of Mineral Resources is inherently uncertain and involves subjective judgments about many relevant factors. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation (including estimated future production from the company’s projects, the anticipated tonnages and grades that will be mined and the estimated level of recovery that will be realized), which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. Mineral Resource estimates may have to be re-estimated based on: (i) fluctuations in copper, nickel, platinum group elements (PGE), gold or other mineral prices; (ii) results of drilling, (iii) metallurgical testing and other studies; (iv) proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receive required permits, approvals and licenses.

Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including, but not limited to, the factors discussed below and under “Risk Factors”, as well as unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labour unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations.

Although the forward-looking statements contained in this release are based upon what management of the company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this release.

The company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of the factors set forth in the “Risk Factors” section and elsewhere in the company’s most recent Management’s Discussion and Analysis report and Annual Information Form, available at www.sedar.com.