English

English Français

Français 日本語

日本語 中文

中文First phase of development envisages an annual production rate

of 100,000 tonnes of copper at a mine-site cash cost of US$0.75/lb copper

KGHM developed controlled convergence room-and-pillar mining method

potentially could provide significant cost savings

KOLWEZI, DEMOCRATIC REPUBLIC OF CONGO – Ivanhoe Mines (TSX: IVN) Executive Chairman Robert Friedland and Chief Executive Officer Lars-Eric Johansson today welcomed the positive findings of an independent pre-feasibility study (PFS) for the first phase of development of the Kamoa Copper Project in the Democratic Republic of Congo (DRC). The Kamoa Copper Project – a joint venture between Ivanhoe Mines and Zijin Mining Group Co., Ltd. – has been independently ranked as the world’s largest, undeveloped, high-grade copper discovery by international mining consultant Wood Mackenzie.

The Kamoa 2016 PFS was independently prepared by OreWin Pty Ltd., Amec Foster Wheeler E&C Services Inc. and SRK Consulting Inc. The report reflects the initial phase of project development and describes the construction and operation of a three-million-tonne-per-annum (Mtpa) underground mine, concentrator processing facility and associated infrastructure. The first phase of mining would target high-grade copper mineralization from shallow, underground resources to yield a high-value concentrate. The planned second phase would entail a major expansion of the mine and mill, and construction of a smelter to produce blister copper.

The Kamoa 2016 PFS includes an economic analysis that is based on Probable Mineral Reserves. A NI 43-101 technical report will be filed on SEDAR at www.sedar.com and on Ivanhoe Mines’ website at www.ivanhoemines.com within 45 days of the issuance of this news release.

Highlights of the Kamoa 2016 PFS:

- Annual mine production of 3 Mtpa at an average grade of 3.86% copper over a 24-year mine life, resulting in annual copper production of approximately 100,000 tonnes.

- Initial capital cost, including contingency, is US$1.2 billion, approximately US$200 million lower than estimated in the Kamoa 2013 PEA.

- Life-of-mine average mine-site cash cost is US$0.75/lb of copper.

- After-tax net present value (NPV) at an 8% discount rate of US$986 million.

- After-tax internal rate of return (IRR) of 17.2% and a payback period of 4.6 years.

- High-grade copper concentrate with an average grade of 39.2% copper and very low arsenic levels.

- Improvements to the mining method have the potential to reduce average mine site cash cost during the first phase to US$0.61/lb of copper, and improve the after-tax NPV at an 8% discount rate to US$1.182 billion, the IRR to 18.9% and the payback period to 4.3 years.

“The results of this independent pre-feasibility study confirm the robustness of the Kamoa Copper Project over a wide range of copper prices, with the potential for significant improvement in the results as we move forward on the Feasibility Study,” said Mr. Friedland.

“We know of no other copper project in the world that offers the potential of multi-decade, large-scale, mechanized production from a near surface, stratiform deposit grading nearly 4% copper, with the demonstrated potential for further high-grade discoveries nearby, and located close to a major mining centre.

“With the support of our partners — including our joint-venture partner, Zijin Mining, our employees, local entrepreneurs and community members, and the DRC government — we are looking forward to building a major new, safe, mechanized copper mine on the western edge of the DRC’s famous Copperbelt.”

The Kamoa 2016 PFS has identified several areas for further evaluation to optimize the project’s economics, including:

- The use of controlled convergence room-and-pillar mining, which has been successfully used by KGHM Polska Miedz S.A. (KGHM) at its copper-mining operations in Poland for the past 20 years. Based on detailed analysis by KGHM Cuprum R&D Centre Ltd., this mining method appears to be well suited to the Kamoa deposit and, if implemented, potentially could provide significant cost savings as there would be no requirement for cemented backfill and ore extraction ratios would increase.

- Increased production up to 4 Mtpa from the proposed initial mining area, with only limited adjustments to the ore-handling and ventilation systems, thereby resulting in a more efficient use of capital.

Kamoa 2016 PFS Results

The base case described in the PFS is the construction and operation of an underground mine, concentrator processing facility and associated infrastructure. The base-case mining rate and concentrator feed capacity is 3 Mtpa. The life-of-mine production scenario schedules 71.9 million tonnes at an average grade of 3.86% copper over 24 years, producing 6.1 million tonnes of copper concentrate, containing approximately 5.3 billion pounds of copper.

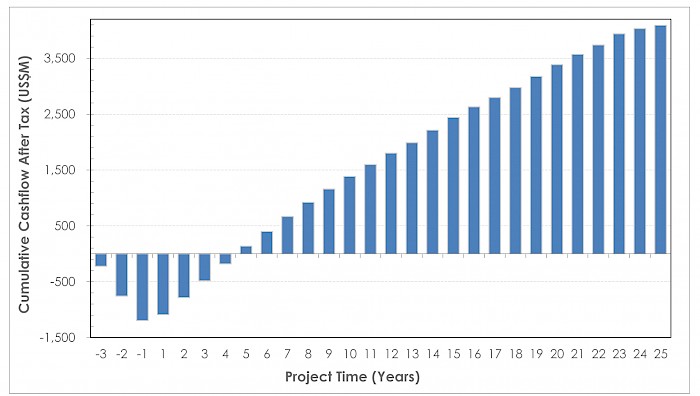

The economic analysis used a long-term price assumption of US$3.00/lb of copper and returns an after-tax NPV at an 8% discount rate of US$986 million. It has an after-tax IRR of 17.2% and a payback period of 4.6 years.

The initial capital cost, including contingency, is US$1.2 billion. The initial capital cost includes a US$104 million advance payment to the DRC state-owned electricity company, SNEL, to upgrade two hydro power plants (Koni and Mwadingusha) to provide Kamoa with access to clean electricity during the initial phase of operations. The upgrading work is being led by Stucky Ltd., of Switzerland, and the advance payment is expected to be recovered through a reduction in the power tariff once Kamoa is in operation. The life-of-mine average mine site cash cost is US$0.75/lb of copper. Key results of the PFS are summarized in Table 1.1.

Table 1.1PFS Results Summary

| Item | Unit | Total |

| Ore Processed (Life of Mine) | ||

| Quantity Ore Treated | kilotonne (kt) | 71,893 |

| Copper Feed Grade | % | 3.86 |

| Concentrate Produced (Life of Mine) | ||

| Copper Concentrate Produced | kt (dry) | 6,106 |

| Copper Recovery | % | 86.36 |

| Copper Concentrate Grade | % | 39.20 |

| Contained Metal in Concentrate | million pounds (Mlb) | 5,277 |

| Contained Metal in Concentrate | kt | 2,394 |

| Key Financial Results | ||

| Initial Capital | US$M | 1,213 |

| Mine-Site Cash Cost | US$/lb Payable Cu | 0.75 |

| Total Cash Cost | US$/lb Payable Cu | 1.48 |

| Site Operating Costs | US$/t ore | 53.22 |

| After-Tax NPV8% | US$M | 986 |

| After-Tax IRR | % | 17.2% |

| Project Payback Period | Years | 4.6 |

Table 1.2 summarizes the financial results and Table 1.3 summarizes mine production and processing statistics.

Table 1.2 Financial Results

| Before Taxation |

After Taxation |

||

| Net Present Value (US $M) | Undiscounted | 5,791 | 4,096 |

| 4.0% | 2,979 | 2,036 | |

| 6.0% | 2,152 | 1,429 | |

| 8.0% | 1,549 | 986 | |

| 10.0% | 1,104 | 657 | |

| 12.0% | 768 | 409 | |

| IRR | – | 20.7% | 17.2% |

| Project Payback (years) | – | 4.1 | 4.6 |

Table 1.3 Mine Production and Processing Statistics

| Item | Unit | Total LOM | Years 1-5 | Years 6-10 | LOM AVG |

| Ore Processed | |||||

| Quantity Ore Treated | kt | 71,893 | 2,934 | 3,008 | 2,996 |

| Copper Feed Grade | % | 3.86 | 4.35 | 4.08 | 3.86 |

| Concentrate Produced | |||||

| Copper Concentrate Produced | kt (dry) | 6,106 | 283 | 271 | 254 |

| Copper Recovery | % | 86.36 | 87.06 | 86.68 | 86.36 |

| Copper Concentrate Grade | % | 39.20 | 39.20 | 39.20 | 39.20 |

| Contained Metal in Concentrate | |||||

| Copper | kt | 2,394 | 111 | 106 | 100 |

| Copper | Mlb | 5,277 | 245 | 234 | 220 |

| Payable Metal | |||||

| Copper | kt | 2,314 | 107 | 103 | 96 |

| Copper | Mlb | 5,102 | 237 | 227 | 213 |

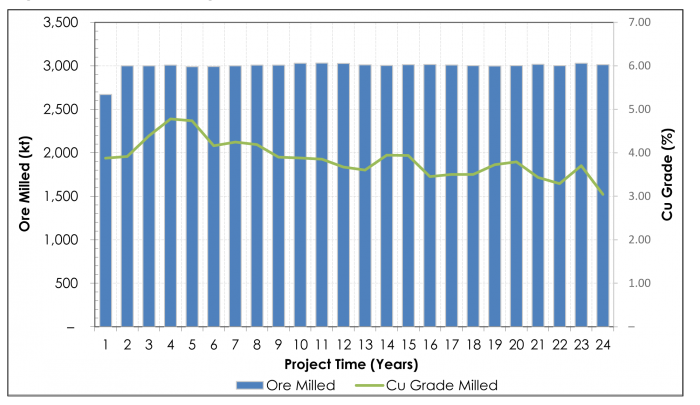

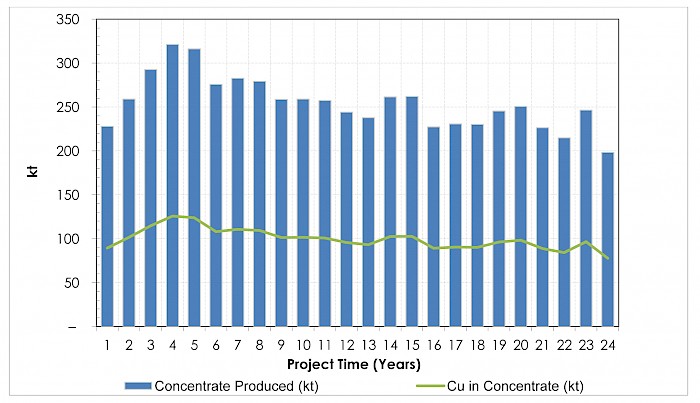

Figures 1.1 and 1.2 depict the processing, concentrate and metal production, respectively.

Figure 1.1 Processing Production

Figure 1.2 Concentrate and Metal Production

Figure by OreWin, February 2016.

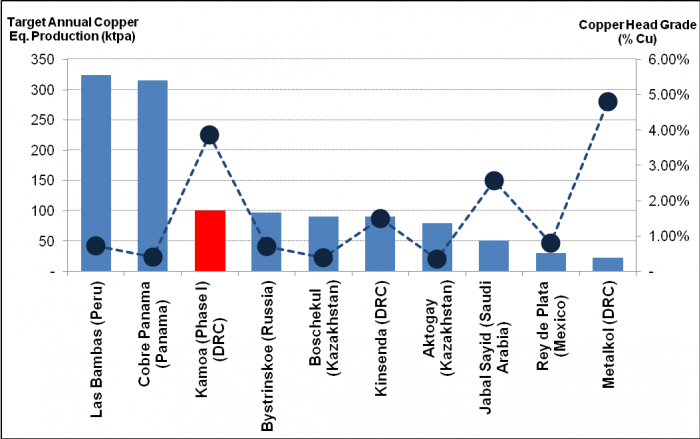

Figure 1.3 Copper Equivalent Production for Highly-Probable Copper Projects Currently Under Construction

Figure based on data from Wood Mackenzie, February 2016. Note: All greenfield development projects classified as “highly probable” by Wood Mackenzie. Source: Wood Mackenzie (based on public disclosure and information gathered in the process of routine research. The Kamoa 2016 PFS has not been reviewed by Wood Mackenzie).

Table 1.4 summarizes unit operating costs and Table 1.5 provides a breakdown of revenue and operating costs. The capital costs for the project are detailed in Table 1.6.

Table 1.4 Unit Operating Costs

| US$/lb Payable Copper | |||

| LOM AVG | Years 1-5 | Years 6-10 | |

| Mine Site | 0.75 | 0.55 | 0.75 |

| Transport | 0.41 | 0.43 | 0.40 |

| Treatment & Refining Charges | 0.18 | 0.18 | 0.18 |

| Royalties & Export Tax | 0.15 | 0.11 | 0.16 |

| Total C1 Cash Cost | 1.48 | 1.27 | 1.48 |

Table 1.5 Revenue and Operating Costs

| Description | TOTAL LOM | YEARS 1-5 | YEARS 6-10 | LOM AVG |

| US$M | US$/t Ore Milled | |||

| REVENUE | ||||

| Copper in Concentrate | 15,305 | 242 | 226 | 213 |

| REALIZATION COSTS | ||||

| Transport | 2,082 | 35 | 30 | 29 |

| Treatment & Refining | 911 | 14 | 13 | 13 |

| Royalties & Export Tax | 748 | 9 | 12 | 10 |

| Total Realization Costs | 3,741 | 58 | 56 | 52 |

| Net Sales Revenue | 11,565 | 184 | 170 | 161 |

| SITE OPERATING COSTS | ||||

| Underground Mining | 2,453 | 25 | 37 | 34 |

| Processing | 886 | 12 | 12 | 12 |

| Tailings | 25 | 0 | 0 | 0 |

| General & Administration | 511 | 8 | 7 | 7 |

| SNEL Discount | -109 | -2 | -2 | -2 |

| Customs | 60 | 1 | 1 | 1 |

| Total Site Operating Costs | 3,826 | 45 | 56 | 53 |

| Operating Margin | 7,738 | 140 | 114 | 108 |

| Operating Margin | 66.9% | 75.8% | 67.0% | 66.9% |

Table 1.6 Capital Investment Summary

| Description | Initial Capital | Sustaining | Total |

| US$M | US$M | US$M | |

| MINING | |||

| Underground Mining | 508 | 499 | 1,007 |

| Subtotal | 508 | 499 | 1,007 |

| POWER | |||

| Power Infrastructure On Site | 19 | 4 | 23 |

| Power Supply Off Site | 104 | – | 104 |

| Subtotal | 123 | 4 | 127 |

| CONCENTRATE & TAILINGS | |||

| Process Plant | 160 | 8 | 167 |

| Tailings | 23 | 62 | 84 |

| Subtotal | 182 | 69 | 252 |

| INFRASTRUCTURE | |||

| Plant Infrastructure | 18 | 4 | 23 |

| Other Infrastructure | 8 | 2 | 10 |

| Owners Camp | 10 | 2 | 12 |

| Contractors Camp | 23 | 5 | 28 |

| Subtotal | 59 | 14 | 73 |

| INDIRECTS | |||

| Engineering, Procurement and Construction Management | 58 | – | 58 |

| Subtotal | 58 | – | 58 |

| OWNERS COST | |||

| Owners Cost | 95 | – | 95 |

| Closure | – | 67 | 67 |

| Subtotal | 95 | 67 | 162 |

| Capital Expenditure before Contingency | 1,025 | 655 | 1,679 |

| Contingency | 189 | 44 | 233 |

| Capital Expenditure after Contingency | 1,213 | 699 | 1,912 |

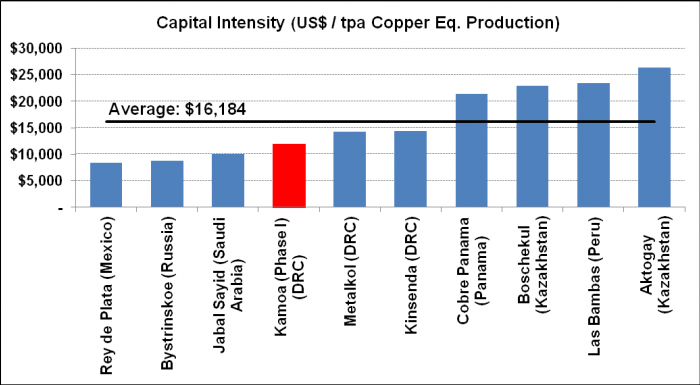

Figure 1.4 Capital Intensity for Highly-Probable Copper Projects Currently Under Construction

Figure based on data from Wood Mackenzie, February 2016. Note: All greenfield development projects classified as “highly probable” by Wood Mackenzie. Source: Wood Mackenzie (based on public disclosure and information gathered in the process of routine research. The Kamoa 2016 PFS has not been reviewed by Wood Mackenzie).

The cash flow sensitivity to metal price variation is shown in Table 1.7 for copper prices from US$2.00/lb to US$4.00/lb.

The sensitivity of after-tax NPV to initial capital cost, direct operating costs, transport and copper feed grade is shown in Table 1.8. The table shows the impact on the base case after-tax NPV8% of US$986M.

Table 1.7 Copper Price Sensitivity

| After Tax NPV (US$M) | Copper Price – US$/lb | ||||

| Discount Rate | 2.00 | 2.50 | 3.00 | 3.50 | 4.00 |

| Undiscounted | 613 | 2,364 | 4,096 | 5,828 | 7,560 |

| 4.0% | -20 | 1,020 | 2,036 | 3,050 | 4,063 |

| 6.0% | -206 | 624 | 1,429 | 2,230 | 3,030 |

| 8.0% | -340 | 336 | 986 | 1,632 | 2,276 |

| 10.0% | -438 | 123 | 657 | 1,187 | 1,714 |

| 12.0% | -508 | -36 | 409 | 851 | 1,289 |

| 15.0% | -579 | -206 | 142 | 486 | 827 |

| IRR | 3.8% | 11.5% | 17.2% | 22.2% | 26.6% |

Table 1.8 Additional Sensitivities

| Change from Base NPV8% (US$M) | |||||||

| Variable | Units | Base Value | -25.0% | -10.0% | – | 10.0% | 25.0% |

| Initial Capital | US$M | 1,213 | 1,252 | 1,092 | 986 | 879 | 720 |

| Direct operating costs per tonne of ore milled | US$/t | 53 | 1,215 | 1,077 | 986 | 894 | 757 |

| Transport costs per tonne of concentrate | US$/t | 356 / 300 | 1,122 | 1,040 | 986 | 931 | 849 |

| Copper feed grade | % Cu | 3.86% | 175 | 662 | 986 | 1,308 | 1,794 |

Figure 1.5 Cumulative Cash Flow

Kamoa Copper Project Description

The Kamoa Copper Project is a very large, stratiform copper deposit with adjacent prospective exploration areas within the Central African Copperbelt, approximately 25 kilometres west of the town of Kolwezi and about 270 kilometres west of Lubumbashi. The Kamoa copper deposit was discovered by Ivanhoe Mines in 2008.

In August 2012, the DRC government granted mining licences to Ivanhoe Mines for the Kamoa Copper Project that cover a total of 400 square kilometres. The licences are valid for 30 years and can be renewed at 15-year intervals. Mine development work at the Kamoa Copper Project began in July 2014 with construction of a box cut for the decline ramps that will provide underground access to the initial high-grade mining area in Kansoko Sud.

Ivanhoe Mines owns a 49.5% interest in Kamoa Holding Limited (Kamoa Holding), an Ivanhoe affiliate that presently owns 95%, on an indirect basis, of the Kamoa Copper Project. Zijin Mining owns a 49.5% interest in Kamoa Holding, which it acquired from Ivanhoe in December 2015 for an aggregate cash consideration of US$412 million. The remaining 1% interest in Kamoa Holding is held by privately-owned Crystal River Global Limited.

A 5%, non-dilutable interest in Kamoa Copper SA, the affiliate that owns the Kamoa Copper Project, was transferred to the DRC government on September 11, 2012, for no consideration, in accordance with the DRC Mining Code. Ivanhoe also has offered to transfer an additional 15% interest to the DRC government on terms to be negotiated. Constructive and cordial negotiations between Ivanhoe Mines, Zijin and senior DRC government officials have been continuing in this regard.

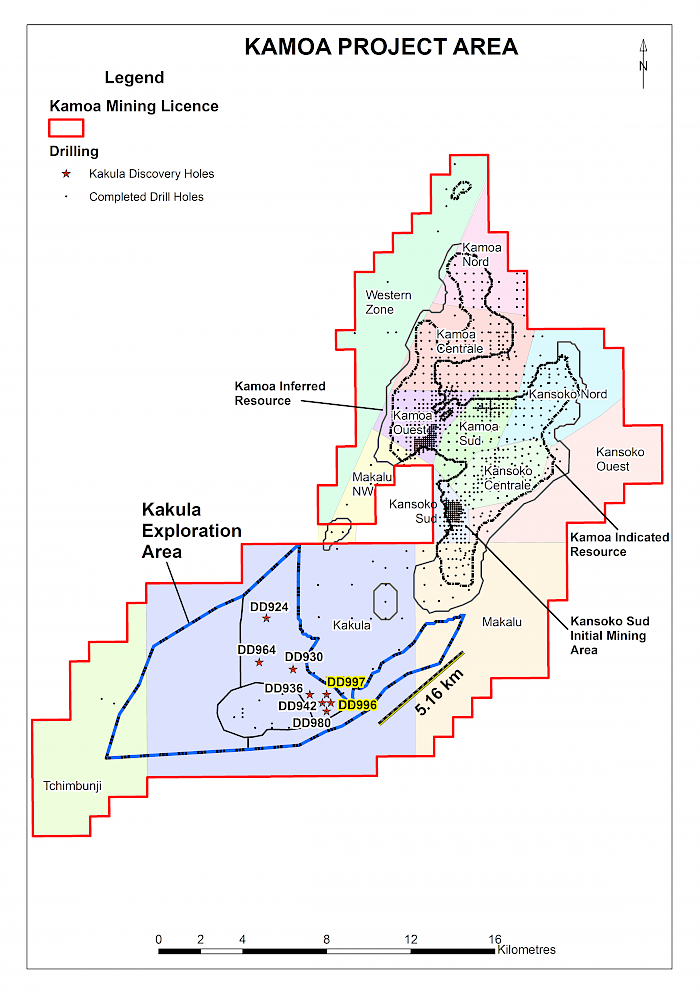

On January 25, 2016, Ivanhoe announced that the Kamoa exploration team made a major new high-grade and flat-lying stratiform copper discovery, named Kakula, located approximately five kilometres southwest of Kamoa’s currently defined resources. The Kakula Discovery is situated within the 400-square-kilometre Kamoa Mining Licence area and represents a major extension of the Kamoa copper deposit, which the company discovered in 2008. Two exploration drill holes completed in late 2015 in the Kakula exploration area – DD996 and DD997 – rank among the highest-grade and highest-grade-thickness intersections drilled to date within the Kamoa Mining Licence area. The Kakula Discovery is not included in the economic analysis of the Kamoa 2016 PFS. Additional details of the Kakula Discovery can be found in Ivanhoe’s January 25, 2016 news release available at www.ivanhoemines.com.

Box cut (portal) at Kamoa’s initial high-grade mining area – Kansoko Sud

Figure 1.6 Kamoa Project map showing the Indicated and Inferred Resource areas, the initial mining area at Kansoko Sud, and the Kakula exploration area

Updated Mineral Resource Estimate

The Mineral Resources have been defined taking into account the 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves. Dr. Harry Parker, SME Registered Member, and Gordon Seibel, SME Registered Member, both employees of Amec Foster Wheeler, are the Qualified Persons for the Mineral Resource estimates. The Mineral Resources at the Kamoa Copper Project have an effective date of May 5, 2014.

Table 1.9 Kamoa Project Indicated and Inferred Mineral Resources (May 2014)

| Category | Tonnage (Mt) |

Area (km2) |

Copper (%) |

True Thickness (m) |

Contained Copper (kt) |

Contained Copper (billions lbs) |

| Indicated | 752 | 52.4 | 2.67 | 5.24 | 20,110 | 44.3 |

| Inferred | 190 | 18.0 | 2.06 | 3.85 | 3,920 | 8.6 |

- 1.Dr. Harry Parker and Gordon Seibel, both RM of SME, are the Qualified Persons for the Mineral Resources, and the effective date of the estimate is May 5, 2014. Mineral Resources are reported inclusive of Mineral Reserves.

- 2.Mineral Resources are reported using a total copper (TCu) cut-off grade of 1% TCu and an approximate minimum assumed thickness of 3 metres. There are reasonable prospects for eventual economic extraction under assumptions of a copper price of US$3.30/lb; employment of underground mechanized room-and-pillar and drift-and-fill mining methods; and that copper concentrates will be produced and sold to a smelter.

- 3.Reported Mineral Resources contain no allowances for hangingwall or footwall contact boundary loss and dilution. No mining recovery has been applied.

- 4.True thickness ranges from 2.0 metres to 17.9 metres for Indicated Mineral Resources and 2.3 metres to 6.6 metres for Inferred Mineral Resources.

- 5.Depth of mineralization below the surface ranges from 10 metres to 1,320 metres for Indicated Mineral Resources and 20 metres to 1,560 metres for Inferred Mineral Resources.

- 6.Approximate drill-hole spacings are 800 metres for Inferred Mineral Resources and 400 metres for Indicated Mineral Resources.

- 7.Tonnage and grade measurements are in metric units. Contained copper tonnes are reported using metric units; contained copper pounds use imperial units. Tonnages are rounded to the nearest million tonnes; grades are rounded to two decimal places.

- 8.Rounding as required by reporting guidelines may result in apparent summation differences between tonnes, grade and contained metal content.

Mineral Reserve

The Kamoa 2016 PFS Mineral Reserve has been estimated by Qualified Person Bernard Peters, Technical Director – Mining, OreWin Pty Ltd. using the 2014 CIM Definition Standards for Mineral Resources and Mineral Reserves to conform to the Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects. The total Mineral Reserve for the Kamoa Project is shown in Table 1.10. The Mineral Reserve is based on the May 2014 Mineral Resource reported in the Kamoa 2016 PFS. The Mineral Reserve is entirely a Probable Mineral Reserve that was converted from Indicated Mineral Resources. The effective date of the Mineral Reserve statement is February 18, 2016.

The production plan defined for the Kamoa 2016 PFS Mineral Reserve represents the first phase of the development plan defined in the Kamoa 2013 PEA. The Kamoa 2013 PEA production scenario assumed that there would be an initial period of concentrate production, followed by an expansion of the mine and concentrator and construction of a smelter.

1.10 Kamoa 2016 PFS Mineral Reserve Statement

| Tonnage (Mt) |

Copper (%) |

Copper (Recovered Mlb) |

Copper (Recovered kt) |

|

| Proven Mineral Reserve | – | – | – | – |

| Probable Mineral Reserve | 71.9 | 3.86 | 5,102 | 2,314 |

| Mineral Reserve | 71.9 | 3.86 | 5,102 | 2,314 |

- The copper price used for calculating the financial analysis is long-term copper at US$3.00/lb. The analysis has been calculated with assumptions for smelter refining and treatment charges, deductions and payment terms, concentrate transport, metallurgical recoveries and royalties.

- For mine planning, the copper price used to calculate block model Net Smelter Returns was US$3.00/lb.

- An elevated cut-off grade of US$100.00/t NSR was used to define the stoping blocks. A marginal cut-off grade of 1% copper was used to defined ore and waste.

- Indicated Mineral Resources were used to report Probable Mineral Reserves.

- The reference point for the Mineral Reserves is mill feed.

- The Mineral Reserves reported above are not additive to the Mineral Resources.

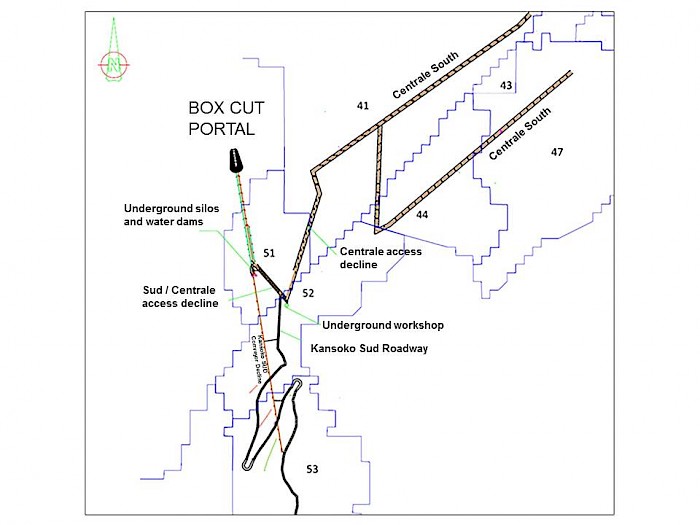

The Kamoa 2016 PFS Mineral Reserve ranges between depths of 170 metres and 1,200 metres below surface and the average dip is approximately 16 degrees. Given the favourable mining characteristics of the Kamoa Mineral Resource, it is considered amenable to large-scale, mechanized, room-and-pillar or drift-and-fill (D&F) mining. The dip and geometry of the resource make it conducive to stepped room-and-pillar (SR&P) mining in the shallow portions of the deposit, transitioning to drift-and-fill mining in the deeper sections. The arrangement of the declines at Kansoko Sud and the Mineral Reserve mining areas are shown in Figure 1.8.

Figure 1.8 Plan showing the Box Cut (portal), the planned declines at Kansoko Sud, and the Mineral Reserve mining areas.

Alternative Mining Method

In parallel with the Kamoa 2016 PFS, an alternative mining method – controlled convergence room-and-pillar mining – was investigated for its suitability for use on the Kamoa deposit. Controlled convergence room-and-pillar mining does not require cemented backfill and instead pillars are stripped to allow the controlled convergence of the backs and floors. This potentially could provide significant cost savings as there is no requirement for cemented backfill and the Mineral Reserve extraction ratios are higher. The controlled convergence room-and-pillar mining method has been successfully implemented by KGHM at its copper mining operations in Poland for the past 20 years.

Ivanhoe engaged KGHM Cuprum R&D Centre Ltd. in early 2015 to study the applicability of this method to Kamoa. The results of the study were received toward the end of 2015 and indicate that the Kamoa deposit is suited to the application of the controlled convergence room-and-pillar mining method. The KGHM Cuprum study suggests that with the completion of the primary and secondary mining, the controlled convergence room-and-pillar mining method is capable of extracting 75% to more than 90% of the in-situ Mineral Reserve.

A sensitivity analysis to the base case Kamoa 2016 PFS economic analysis is shown in Table 1.11, where capital and operating costs associated with cemented backfill have been excluded and the in-situ Mineral Reserve extraction ratio has been increased.

Table 1.11 Mining Method Comparison – Overall Results

| Item | Unit | SR&P and D&F (With Fill) |

Controlled Convergence Room-and-Pillar (No Fill) |

| Ore Processed | PFS Base Case | PFS Sensitivity | |

| Quantity Ore Treated | kt | 71,893 | 71,893 |

| Copper Feed Grade | % | 3.86 | 3.86 |

| Concentrate Produced | |||

| Copper Concentrate Produced | kt (dry) | 6,106 | 6,106 |

| Copper Recovery | % | 86.36 | 86.36 |

| Copper Concentrate Grade | % | 39.20 | 39.20 |

| Payable Copper | Mlb | 5,102 | 5,102 |

| Key Financial Results | |||

| Initial Capital | US$M | 1,213 | 1,155 |

| Mine Site Cash Cost | US$/lb Payable Cu | 0.75 | 0.61 |

| Total Cash Cost | US$/lb Payable Cu | 1.48 | 1.35 |

| Site Operating Costs | US$/t ore | 53.22 | 43.54 |

| After Tax NPV8% | US$M | 986 | 1,182 |

| After Tax IRR | % | 17.2% | 18.9% |

| Project Payback Period | Years | 4.6 | 4.3 |

Metallurgical Test Work and Concentrator Design

Between 2010 and 2015, a series of metallurgical test work programs were completed on drill core samples of known Kamoa copper mineralization. These investigations focused on metallurgical characterization and flow-sheet development for the processing of hypogene and supergene copper mineralization.

Bench-scale metallurgical flotation test work carried out at XPS Consulting and Testwork Services laboratories in Falconbridge, Ontario, Canada, has shown positive results. The most recent work was conducted on composite samples of drill core from the Kansoko Sud and Kansoko Centrale areas in the southern part of the Kamoa Mineral Resource area. Two master composite samples were formulated; one representative of the first four to five years of planned mine production, and the second representative of years five to fifteen of mine production. Test work on the master composite representative of the early years of mining, and grading 3.61% copper, produced a copper recovery of 85.4% at a concentrate grade of 37.0% copper. Material from the later years of mining, and grading 3.20% copper, produced a copper recovery of 89.2% at a concentrate grade of 35.0% copper using the same flowsheet.

Average arsenic levels in the concentrate were measured to be approximately 0.02%, which is significantly lower than the limit of 0.5% imposed by Chinese smelters. Very low arsenic levels in concentrate are expected to attract a premium from copper-concentrate traders.

The concentrator design incorporates a run-of-mine stockpile, followed by primary and secondary crushing on surface. The crushed material with a design size distribution of 80% passing (or p80) 9 millimetres (mm), is fed into a two-stage ball milling circuit for further size reduction to a target grind size p80 of 53 micrometres (µm). The milled slurry is subjected to rougher flotation followed by scavenger flotation. The high-grade, or fast-floating rougher concentrate, and medium-grade or slow-floating scavenger concentrate are collected separately. The rougher concentrate is upgraded in two stages of cleaning to produce a high-grade increment to final concentrate. The medium-grade scavenger concentrate and tailings from the two rougher cleaning stages are combined and re-ground to a p80 of 10µm before being cleaned in two stages. The cleaned scavenger concentrate then is combined with the cleaned rougher concentrate to form the final concentrate. The final concentrate is thickened before being pumped to the concentrate filter. Filter cake then is bagged for shipment to market.

Electric Power

Electric power for the Kamoa Copper Project is planned to be sourced from three hydro power plants: Koni, Mwadingusha and Nzilo 1. A financing agreement with SNEL has been finalized for upgrading these plants to secure a long-term, clean, sustainable power supply to meet the requirements of Kamoa’s planned mine and smelter development.

The Kamoa 2016 PFS initial capital cost of US$1.2 billion includes a US$104 million advance payment to SNEL to upgrade two of the hydro-power plants, Koni and Mwadingusha, to provide Kamoa with hydro-electric power during the initial phase of operations. The upgrading work is being led by Stucky Ltd. and the advance payment is expected to be recovered through a reduction in the power tariff once Kamoa is in operation. Kamoa initially will be powered by existing capacity on the national grid and on-site diesel generators, until upgrading work on the hydro-power plants has been completed.

Transportation

A phased logistics solution is proposed in the Kamoa 2016 PFS. Initially the corridor between southern DRC and Durban in South Africa is viewed as the most attractive and reliable export route. As soon as the railroad between Kolwezi and Dilolo, a town near the DRC-Angolan border, is rehabilitated, Kamoa’s production is expected to be transported by rail to the port of Lobito in Angola.

Qualified persons, Quality Control and Assurance

The following companies have undertaken work in preparation of the Kamoa 2016 PFS:

- OreWin – Overall report preparation, mining, Mineral Reserve estimation and economic analysis.

- Amec Foster Wheeler – Mineral Resource estimation, processing and infrastructure.

- SRK Consulting – Mine geotechnical recommendations.

The independent Qualified Persons responsible for preparing the Kamoa 2016 PFS, on which the technical report will be based include Bernard Peters (OreWin); Dr. Harry Parker (Amec Foster Wheeler); Gordon Seibel (Amec Foster Wheeler); Dean David (Amec Foster Wheeler); and William Joughin (SRK). Each Qualified Person has reviewed and approved the information in this news release relevant to the portion of the Kamoa 2016 PFS for which they are responsible.

Other scientific and technical information in this news release has been reviewed and approved by Stephen Torr, P.Geo., Ivanhoe Mines’ Vice President, Project Geology and Evaluation, a Qualified Person under the terms of National Instrument 43-101. Mr. Torr has verified the technical data disclosed in this news release.

Ivanhoe Mines maintains a comprehensive chain of custody and QA-QC program on assays from its Kamoa Copper Project. Half-sawn core is processed at its on-site preparation laboratory in Kamoa, prepared samples then are shipped by secure courier to Bureau Veritas Minerals (BVM) Laboratories in Australia, an ISO17025 accredited facility. Copper assays are determined at BVM by mixed-acid digestion with ICP finish. Industry-standard certified reference materials and blanks are inserted into the sample stream prior to dispatch to BVM. For detailed information about assay methods and data verification measures used to support the scientific and technical information, please refer to the current technical report on the Kamoa Copper Project on the SEDAR profile of Ivanhoe Mines at www.sedar.com.

Ivanhoe Mines will be filing a current NI 43-101 Technical Report on the Kamoa Copper Project within 45 days of this news release.

Data Verification

Amec Foster Wheeler reviewed the sample chain of custody, quality assurance and control procedures, and qualifications of analytical laboratories. Amec Foster Wheeler is of the opinion that the procedures and QA/QC control are acceptable to support Mineral Resource estimation. Amec Foster Wheeler also audited the assay database, core logging, and geological interpretations on a number of occasions between 2009 and 2015, and has found no material issues with the data as a result of these audits.

In the opinion of the Amec Foster Wheeler Qualified Persons, the data verification programs undertaken on the data collected from the Project support the geological interpretations. The analytical and database quality and the data collected can support Mineral Resource estimation.

About Ivanhoe Mines

Ivanhoe Mines is advancing and developing its three principal projects:

- The Kamoa Copper Discovery in a previously unknown extension of the Central African Copperbelt in the DRC’s Lualaba Province.

- The Platreef Discovery of platinum, palladium, nickel, copper, gold and rhodium on the Northern Limb of the Bushveld Complex in South Africa.

- The historic, high-grade Kipushi zinc-copper mine, also on the Copperbelt in the DRC.

Information contacts

Investors

Bill Trenaman +1.604.331.9834

Media

North America: Bob Williamson +1.604.512.4856

South Africa: Jeremy Michaels +27.82.939.4812

Cautionary statement on forward-looking information

Certain statements in this release constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws, including without limitation, the timing and results of: (i) the timing and terms of transfer of an additional 15% interest in the Kamoa Copper Project to the DRC government; (ii) all of the results of the pre-feasibility study; (iii) the use of the alternative controlled convergence room-and-pillar mining method; (iv) increased production in subsequent phases of up to 4 Mtpa; (v) the expectation that concentrate with very low arsenic levels to attract a premium from traders; (vi) the expectation that Kamoa’s production is to be transported by rail to the port of Lobito once the the railroad between Kolwezi and Dilolo is rehabilitated; (vii) the expectation that the advance payment to SNEL will be recovered through a reduction in the power tariff once Kamoa is in operation; and (viii) the delineation of a mineral resource at the Kakula exploration target. Such statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as “may”, “would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate”, “scheduled”, “forecast”, “predict” and other similar terminology, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. These statements reflect the company’s current expectations regarding future events, performance and results and speak only as of the date of this release.

As well, all of the results of the pre-feasibility study of the Kamoa Project constitute forward-looking information, including estimates of internal rates of return (including an after tax internal rate of return of 17.2% with a payback period of 4.6 years), net present value (including a project NPV of US$986 million at an 8% discount rate), future production (including an annual production rate of 100,000 tonnes of copper in the first phase of development), estimates of cash cost (including mine site cash cost of US$0.75/lb and C1 cash cost per pound of US$1.48), assumed long term price for copper of US$3.00 per pound, proposed mining plans and methods (including the potential to use the alternate controlled convergence room-and-pillar mining method, mine life estimates, cash flow forecasts, metal recoveries, and estimates of capital and operating costs (including initial capital costs of US$1.2 billion). Furthermore, with respect to this specific forward-looking information concerning the development of the Kamoa Project, the company has based its assumptions and analysis on certain factors that are inherently uncertain. Uncertainties include among others: (i) the adequacy of infrastructure (including the rehabilitation of the Koni, Mwadingusha and Nzilo 1 hydroelectric power plants); (ii) unforeseen changes in geological characteristics; (iii) metallurgical characteristics of the mineralization; (iv) the ability to develop adequate processing capacity; (v) the price of copper; (vi) the availability of equipment and facilities necessary to complete development; (vii) the cost of consumables and mining and processing equipment; (viii) unforeseen technological and engineering problems; (ix) accidents or acts of sabotage or terrorism; (x) currency fluctuations; (xi) changes in laws or regulations; (xii) the availability and productivity of skilled labour; (xiii) the regulation of the mining industry by various governmental agencies; and (xiv) political factors.

This release also contains references to estimates of Mineral Resources and Mineral Reserves. The estimation of Mineral Resources is inherently uncertain and involves subjective judgments about many relevant factors. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation (including estimated future production from the Kamoa Project, the anticipated tonnages and grades that will be mined and the estimated level of recovery that will be realized), which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. Mineral Resource estimates may have to be re-estimated based on: (i) fluctuations in copper price; (ii) results of drilling, (iii) metallurgical testing and other studies; (iv) proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receive required permits, approvals and licenses. Mineral Reserves are also disclosed in this release. Mineral Reserves are those portions of Mineral Resources that have demonstrated economic viability after taking into account all mining factors. Mineral Reserves may, in the future, cease to be a Mineral Reserve if economic viability can no longer be demonstrated because of, among other things, adverse changes in commodity prices, changes in law or regulation or changes to mine plans.

Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including, but not limited to, the factors discussed here, as well as unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social, political or labour unrest; changes in commodity prices (and copper in particular); limitations and availability of capital; and the failure of exploration programs or studies to deliver anticipated results (including the actual results of drilling and exploration activities), or results that would justify and support continued exploration, studies, development or operations.

Although the forward-looking statements contained in this release are based upon what management of the company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this release.

The company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of the factors set forth in the “Risk Factors” section and elsewhere in the company’s most recent Management’s Discussion and Analysis report and Annual Information Form, available at www.sedar.com.